The Silent Killer Nobody Talks About at Demo Day

Every pitch deck at Demo Day shows the same hockey stick. Revenue climbing. Users multiplying. Logos stacking up like trophies.

But here's what investors see that founders often miss: the math underneath. Specifically, whether each new customer actually makes the company money or slowly bleeds it dry.

This is the domain of unit economics: the fundamental calculation of whether your business model actually works at the individual customer level. Get this wrong, and growth becomes a treadmill that speeds up until you fall off.

What Unit Economics Actually Measures

At its core, unit economics answers one question: Does acquiring a customer generate more value than it costs?

Two metrics sit at the center of this calculation:

Customer Acquisition Cost (CAC) represents everything you spend to acquire a single customer. Marketing spend, sales salaries, tools, content production, advertising. Add it all up and divide by new customers acquired. That's your CAC.

Lifetime Value (LTV) represents the total gross profit a customer generates over their entire relationship with your company. For SaaS, the formula is average revenue per account × gross margin % ÷ monthly churn rate. The gross margin adjustment is not optional: the standard 3:1 benchmark assumes margin-adjusted LTV, and skipping it quietly inflates your ratio. Two caveats. Dividing by churn assumes your churn rate stays constant forever, and at low churn it produces fantasy lifetimes (2% monthly churn implies a 50-month average lifetime that few startups have been alive long enough to observe). And the whole calculation is only as honest as the margin underneath it, which is why the contribution margin section below matters.

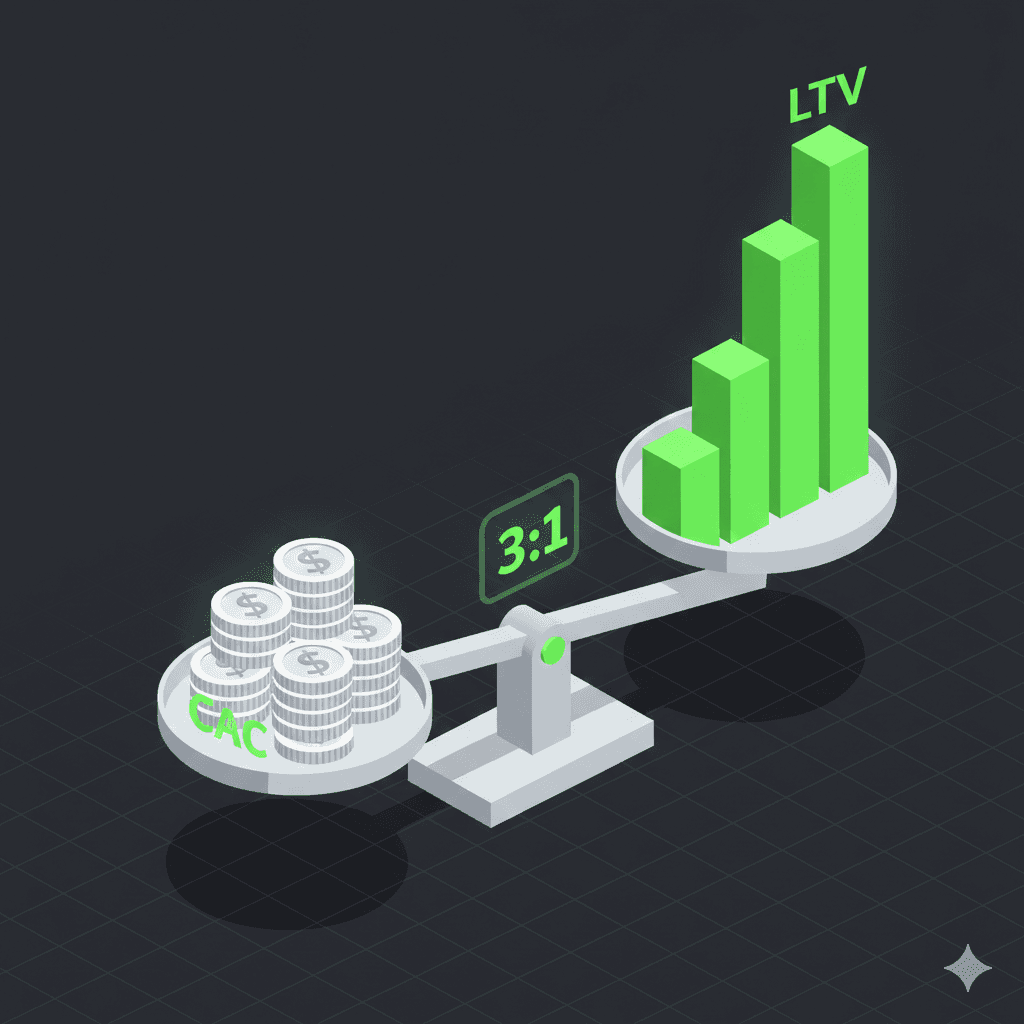

The relationship between these two numbers, expressed as the LTV:CAC ratio, tells you whether your growth engine creates value or destroys it.

The 3:1 Benchmark and Why Context Matters

The commonly cited benchmark is an LTV:CAC ratio of 3:1 or higher. For every dollar spent acquiring a customer, you should generate at least three dollars in lifetime value.

A quick worked example. Say your average customer pays $500 per month, your gross margin is 80%, and monthly churn is 2.5%. LTV = $500 × 0.80 ÷ 0.025 = $16,000. If it costs $4,000 to acquire that customer, the LTV:CAC ratio is 4:1, and CAC payback is $4,000 ÷ ($500 × 0.80) = 10 months. Healthy on both counts.

But this benchmark requires context. At Seed stage, ratios below 3:1 might be acceptable if you're still optimizing your acquisition channels. By Series A, investors expect to see a clear path to 3:1 or better. By Series B, anything below 3:1 raises serious questions about scalability.

A ratio of 1:1 means you're spending a dollar to make a dollar. That's not a business; it's an expensive hobby. Below 1:1, every customer you acquire costs more than they will ever return. You're funding their usage out of your own pocket.

Ratios above 5:1 might seem like cause for celebration, but they often indicate underinvestment in growth. You're leaving acquisition opportunities on the table. For ecommerce founders where the inputs are messier (multi-channel attribution, variable COGS, seasonal distortion), see our dedicated guide to CAC, LTV, and payback period for ecommerce.

CAC Payback: The Cash Flow Reality Check

LTV:CAC ratio tells you whether the math works over time. CAC payback period tells you whether you'll survive long enough to see that time.

CAC payback measures how many months it takes to recover your customer acquisition cost from the gross margin generated by that customer. The formula: CAC divided by (Monthly Revenue per Customer × Gross Margin %).

Why does this matter? Because even with a healthy LTV:CAC ratio, a long payback period can kill your cash flow. If it takes 24 months to recover CAC, you need enough runway to fund all customer acquisition until those customers start contributing positive margin.

For most SaaS companies, the target is 12 to 18 months CAC payback. Below 12 months is excellent. Above 18 months creates significant cash pressure. Above 24 months, you're building a business that requires constant capital infusion to grow.

How Zombie Companies Get Created

Zombie companies don't announce themselves. They emerge gradually from founders who optimize for growth metrics while ignoring unit economics.

The pattern typically looks like this: Early traction creates pressure to grow faster. The team increases ad spend and expands the sales team. Customer count rises. Revenue rises. Everyone celebrates.

But underneath, CAC creeps up as the easiest customers get acquired first. Churn increases as less-qualified customers sign up. Burn rate accelerates. The LTV:CAC ratio deteriorates.

By the time the problem becomes obvious, the company is stuck. Too much burn to survive without new funding. Unit economics too weak to attract investors. Not enough margin to self-fund growth.

This is the zombie state: technically alive, growing slowly or not at all, unable to reach profitability or raise capital. The business limps forward until the money runs out.

The Contribution Margin Foundation

Before obsessing over LTV:CAC, ensure you understand contribution margin. This measures the revenue remaining after variable costs associated with delivering your product.

For SaaS, variable costs typically include hosting, payment processing, and customer success costs that scale with usage. For ecommerce, add COGS, shipping, and fulfillment.

Contribution margin matters because it determines how much of each revenue dollar actually flows toward recovering CAC and generating profit. A company with 80% contribution margin recovers CAC much faster than one with 50% margin, even at identical revenue levels.

If your contribution margin is negative, no amount of growth will save you. You're losing money on every transaction. Fix the margin first, then focus on acquisition.

Stage-Appropriate Expectations

Pre-Seed to Seed: Unit economics might be unclear or unfavorable. That's acceptable. Your job is to find product-market fit. But you should be measuring these numbers and tracking their trajectory. Investors will ask.

Seed to Series A: You need demonstrable unit economics with a clear improvement trend. LTV:CAC should be approaching 3:1. CAC payback should be under 18 months. If the numbers aren't there yet, you need a credible story for how they'll improve.

Series A and Beyond: Unit economics must be proven and defensible. Investors at this stage scrutinize these numbers carefully. Weak unit economics will either kill the round or result in punishing terms.

The Metrics That Feed Into Unit Economics

Unit economics don't exist in isolation. They connect to a web of supporting metrics that provide context and levers for improvement.

MRR and ARR provide the revenue foundation. Net Revenue Retention reveals whether existing customers expand or contract over time, directly impacting LTV. Gross Revenue Retention isolates the churn impact from expansion.

Expansion revenue can dramatically improve LTV without increasing CAC. If customers consistently upgrade or purchase additional products, your LTV calculation expands significantly.

The Magic Number measures sales efficiency: how much new ARR you generate for every dollar spent on sales and marketing. As a rule of thumb, scores above 0.75 indicate efficient growth; below 0.5 suggests you're burning cash for growth.

Efficiency Metrics for the Current Environment

The era of growth-at-all-costs is over. Investors now prioritize efficient growth, measured through metrics like Burn Multiple and the Rule of 40.

Burn Multiple divides net burn by net new ARR. A burn multiple of 1x means you're spending one dollar to generate one dollar of new ARR. The usual rules of thumb: below 1x is exceptional, above 2x raises concerns, and above 3x signals serious inefficiency.

Rule of 40 adds your year-over-year growth rate to your profit margin (we recommend free-cash-flow margin, since it reflects what your burn actually shows). As a rule of thumb, the sum should equal or exceed 40. A company growing 30% with a 10% FCF margin passes. One growing 50% with a negative 20% FCF margin fails.

These efficiency metrics connect directly to unit economics. Strong unit economics make efficient growth possible. Weak unit economics force you to choose between growth and survival.

The Cash Flow Connection

Unit economics ultimately determine cash flow. Strong unit economics with short payback periods generate cash that funds further growth. Weak unit economics with long payback periods drain cash continuously.

Working capital requirements also factor in. If you invoice annually upfront (common in enterprise SaaS), your cash position improves relative to monthly billing. If you carry inventory (ecommerce), cash gets tied up before you see revenue.

The goal is reaching break-even point where operating cash flow covers all costs, or generating free cash flow that accumulates over time. Unit economics determine whether and when that's possible.

Practical Steps for Founders

1. Calculate your numbers today. Even rough estimates are better than flying blind. Use your last three months of data to calculate CAC, estimate LTV based on current churn and revenue, and compute the ratio.

2. Track monthly. Unit economics change as you scale, enter new markets, and adjust pricing. What worked at $50K MRR might break at $500K MRR. Build a dashboard that updates regularly.

3. Segment aggressively. Blended unit economics hide important truths. Break down CAC by channel, LTV by customer segment, and payback by product tier. The segments often tell different stories.

4. Model scenarios. What happens to unit economics if churn increases 2%? If you raise prices 15%? If CAC increases with scale? Build models that let you stress-test assumptions.

5. Connect to fundraising narrative. Investors will ask about unit economics. Prepare clear answers with supporting data. If the numbers aren't where they need to be, have a credible improvement plan.

The Discipline That Separates Outcomes

The difference between companies that scale successfully and those that become zombies often comes down to when founders start paying attention to unit economics.

Wait too long, and you've built a growth engine on a broken foundation. The math never works no matter how fast you grow.

Start early, and you build discipline into your company's DNA. Every growth initiative gets evaluated through the lens of unit economics. Every pricing decision considers LTV impact. Every marketing channel gets measured against CAC contribution.

This discipline doesn't guarantee success. Markets shift, competition intensifies, products fail. But it does prevent the most common mode of startup death: growing yourself into a corner where the math never worked and you just didn't see it until too late.

Unit economics aren't just investor metrics. They're the fundamental proof that your business model works. Get them right early, and you give yourself the foundation for everything that comes next.

For a step-by-step guide to building the bookkeeping foundation that produces reliable unit economics data, see our complete guide to bookkeeping for startups.