Most founders treat fundraising like a job interview. You prepare your story, rehearse your answers, and hope the person across the table likes you enough to say yes.

VCs don't see it that way. They're not hiring you. They're constructing a portfolio. Every check they write needs to have a plausible path to returning the entire fund. Your startup isn't being evaluated on its own merits alone. It's being compared to every other opportunity on the partner's desk that week.

This mismatch in mental models explains most rejections. Not bad ideas. Not weak teams. Just founders who don't understand the game they're playing.

This guide covers how VCs actually think, how their funds work, and what that means for how you should approach your raise. Not theory. Mechanics.

What VCs Actually Do All Day

If you think a VC's job is to sit in pitch meetings and write checks, you're seeing maybe 15% of it. Understanding how they spend their time explains why your fundraise moves the way it does.

Deal sourcing consumes a massive chunk of the week. Partners are scanning inbound applications, working their referral networks, attending events, and doing outbound research on companies they've heard about secondhand. The best firms have systems for this. Associates and analysts triage hundreds of decks so partners only see the most promising ones.

Portfolio support is the other major time commitment. Once a VC invests, they're on your board or at least in your corner. That means helping with hiring, making customer intros, advising on strategy, and troubleshooting when things go sideways. A partner with 8-10 active board seats has limited bandwidth for new deals.

LP management is the part founders never see. VCs raise money from limited partners: endowments, pension funds, family offices, fund-of-funds. Those LPs expect regular updates, quarterly reports, and annual meetings. Fund administration, compliance, and reporting are real work.

Partner meetings and investment committee are where decisions get made. At most firms, no single partner can write a check unilaterally. Deals go through an internal process: a championing partner presents the opportunity, other partners ask hard questions, and the group decides. Understanding this dynamic matters because the partner you're pitching has to turn around and sell your company internally.

The key insight for founders: a typical VC sees 1,000+ companies per year and invests in 5-10. Their job is to say no efficiently. When you understand that, you stop taking rejection personally and start thinking about how to be one of the few that make it through the filter.

How a VC Fund Is Structured

You can't negotiate well with someone whose incentives you don't understand. Here's how the money actually works.

The LP/GP Model

A venture capital fund is a legal entity, usually a limited partnership. The general partners (GPs) are the VCs who make investment decisions. The limited partners (LPs) are the institutions and individuals who provide the capital.

LPs commit a fixed amount of money to the fund. They don't hand it over all at once. Capital is "called" as the GPs find deals to invest in. In return, LPs expect the fund to return significantly more than they put in.

GPs earn money two ways: management fees (typically 2% of committed capital per year, used to cover salaries and operations) and carried interest (typically 20% of profits above a certain return threshold). This is the "2 and 20" model you've probably heard referenced.

The Fund Lifecycle

Every fund has a defined lifespan, usually 10 years with possible extensions. The lifecycle looks like this:

Years 1-3: Deployment. The fund is actively investing in new companies. This is when you want to be fundraising from them. The fund has dry powder and is looking for deals.

Years 4-7: Management. The fund slows or stops new investments and focuses on supporting existing portfolio companies. Follow-on investments in winners happen here.

Years 8-10: Harvest. The fund needs liquidity events (acquisitions, IPOs) to return capital to LPs. Pressure increases on portfolio companies to find exits.

Why This Matters for You

Fund size dictates check size. A $100M fund can't write $50M checks. A $500M fund can't spend time on $500K deals. Most funds invest 1-3% of total fund size per initial check. If you're raising a $2M seed round, you're looking for funds in the $50-150M range.

Fund stage dictates urgency. A fund in year one has time and capital. A fund in year seven is under pressure to show returns. The partner's enthusiasm for your deal is filtered through where their fund sits in its lifecycle.

A VC's incentives are not identical to yours. You want to build a great company. They need to return 3x+ to their LPs within the fund's lifetime. Those goals overlap most of the time, but they diverge in important moments, especially around exit timing and growth-at-all-costs decisions.

The VC Investment Process, Stage by Stage

The venture capital investment process follows a predictable arc. Knowing where you are in it, and what triggers movement to the next stage, lets you fundraise with intention instead of anxiety.

Stage 1: Initial Outreach and Sourcing

This is how you get on their radar. Three paths exist:

Warm introductions remain the highest-conversion channel. A referral from a portfolio founder, a trusted angel, or a mutual connection gets your deck moved to the top of the stack. This isn't about nepotism. It's signal. If someone the VC trusts vouches for you, it reduces the risk of wasting time.

Cold outreach can work but the hit rate is low. If you go this route, your email needs to be specific: why this firm, why this partner, why now. Generic "we're disrupting X" emails get deleted.

Inbound through content and presence. Some founders get noticed because they're visible: writing about their space, speaking at events, building in public. VCs are constantly scanning for signal.

Typical timeline: Getting from outreach to a first meeting takes anywhere from one day (warm intro to a firm actively looking) to never (cold email to a fund that's fully deployed).

Stage 2: First Meeting and Deck Review

The first meeting is 30-45 minutes, and it's not a decision point. The VC is doing one thing: pattern matching. Does this founder, market, and traction profile match what they're looking for?

You'll walk through your deck. They'll ask questions. The meeting will feel either energizing or flat. What you're looking for is genuine curiosity and follow-up questions that go deeper, not just polite nodding.

What happens after: If interested, the partner will do some quick homework: market research, competitive landscape, reference calls. If they want to proceed, they'll schedule a deeper dive or introduce you to other partners.

Typical timeline: 1-2 weeks between first meeting and a decision to continue or pass.

Stage 3: Partner Meeting

This is the internal sell. The championing partner brings your deal to the full partnership. At some firms, you'll present directly. At others, the partner presents on your behalf using your materials.

This is where many promising deals die. The championing partner might love you, but if two other partners have concerns about the market or a competing portfolio company, it stalls.

What you can do: Give your champion the ammunition they need. Data, customer references, market analysis. Anything that helps them answer the hard questions their partners will ask.

Typical timeline: 1-3 weeks, depending on the firm's meeting cadence.

Stage 4: Term Sheet

If the partnership decides to move forward, you'll receive a term sheet, a non-binding document outlining the proposed investment terms. This covers valuation, investment amount, board seats, liquidation preferences, anti-dilution provisions, and other governance terms.

A term sheet is a soft yes. It means they want to do the deal, subject to due diligence confirming that everything you've told them is true.

Typical timeline: Term sheet negotiation takes 1-2 weeks. Don't rush this. Have a lawyer who's done venture deals before.

Stage 5: Due Diligence

With a signed term sheet, the VC goes deep. This stage is covered in detail in the next section.

Typical timeline: 2-6 weeks, depending on deal complexity and how prepared you are.

Stage 6: Close

Legal documents are drafted, signed, and funds are wired. This involves converting the term sheet into definitive agreements: stock purchase agreement, investor rights agreement, voting agreement, and right of first refusal agreement.

Typical timeline: 2-4 weeks after diligence completes.

Total timeline from first meeting to money in the bank: 6-16 weeks is typical. Some deals close faster. Many take longer. The fastest I've seen is three weeks. The slowest drag on for months before either closing or dying.

What VCs Look for in a Startup

When a VC evaluates your company, they're running a mental model against a specific set of criteria. Here's what actually drives their decision.

Market Size

VCs need billion-dollar outcomes because of portfolio math. If a fund invests in 25 companies and expects 2-3 winners to return the entire fund, each winner needs to return 10-30x. A $5M investment needs to become $50-150M at exit. That only happens in large markets.

This doesn't mean you need to be going after a trillion-dollar TAM. It means you need to show a credible path to being a $100M+ revenue company. If the ceiling on your business is $20M in annual revenue, VCs won't be interested. Not because it's a bad business, but because it doesn't fit their return model.

Team and Founder-Market Fit

Why are you the right person to build this? This isn't about credentials. It's about unfair advantages. Deep domain expertise, unique access to customers, technical skills that would take competitors years to replicate, or lived experience with the problem.

VCs also evaluate your ability to recruit. Can you attract A-players? Building a company is a team sport, and a solo founder with no network is a higher-risk bet.

Traction and Signal

At pre-seed, traction might be a waitlist, design partners, or a compelling prototype with early user feedback. At seed, investors want to see revenue, ideally MRR with month-over-month growth. By Series A, you need meaningful ARR, strong retention, and a repeatable acquisition channel.

The numbers matter less than the trajectory. $50K MRR growing 20% month-over-month is more exciting than $200K MRR that's been flat for six months.

Business Model and Unit Economics

Can you make money? And does the model get better or worse as you scale? VCs want to see a path to strong gross margins (70%+ for SaaS) and improving unit economics over time.

If your CAC is $500 and your LTV is $5,000, that's a 10:1 ratio, and it's compelling. If your CAC is $500 and your LTV is $600, you're running on fumes. For a deeper dive into the specific financial metrics Series A investors scrutinize, read our breakdown of the five metrics every Series A investor actually cares about.

Competitive Moat

What stops a well-funded competitor from copying you? Network effects, proprietary data, switching costs, regulatory advantages, or deep technical IP. "We're faster" or "our UX is better" are not moats. They're temporary advantages that can be replicated.

The key insight: VCs are not evaluating your company in isolation. They're comparing it to every other deal on their desk that week. You don't need to be perfect. You need to be the most compelling risk-adjusted opportunity in a competitive set.

The Due Diligence Process

Due diligence is triggered by a soft yes, usually a signed term sheet. Think of it as the VC verifying that everything you've represented is accurate before wiring the money.

What VCs Examine

Financials. Your P&L, cash flow statement, balance sheet, and historical financial data. They're looking for consistency with what you presented, clean accounting, and no surprises. They'll scrutinize your burn rate, runway calculations, and revenue recognition.

Cap table. Every SAFE, convertible note, equity grant, and option pool. They want to understand the fully diluted ownership structure and ensure there are no hidden obligations. If your cap table is a mess (multiple SAFEs at different caps with unclear conversion terms), it slows everything down. Our deep dive on how multiple SAFEs dilute your cap table covers the mechanics.

Legal. Corporate formation documents, IP assignments, employment agreements, customer contracts, and any pending or threatened litigation. VCs want to confirm that the company owns its IP, employees have proper agreements, and there are no legal landmines.

Customer references. Expect VCs to talk to 3-5 of your customers directly. They'll ask about implementation experience, competitive alternatives considered, likelihood of renewal, and willingness to expand. Cherry-picking your happiest customers is fine, but sophisticated VCs will also ask for customers you didn't suggest.

Team and background. Reference checks on founders and key executives. They'll talk to former colleagues, investors, and anyone who can speak to your character, work ethic, and ability to execute under pressure.

Common Reasons Deals Die in Diligence

Financial inconsistencies. The numbers in your deck don't match your actual books. Revenue was overstated. Churn was hidden. Burn rate was understated. This is the fastest way to kill a deal and your reputation.

Cap table complexity. Too many SAFEs at varying terms, unclear conversion mechanics, or missing documentation. It's not a dealbreaker by itself, but it adds legal cost and delay.

Customer concentration. If 60% of your revenue comes from one customer, that's a risk VCs will price in heavily, or walk away from.

IP issues. Code written by a contractor without a proper assignment agreement. A co-founder who left without signing over their IP. These create existential legal risk.

Reference red flags. A customer who's lukewarm, a former employee who raises concerns, or a co-founder reference that doesn't align with what you told the VC.

What to Have Ready Before Diligence Starts

The founders who close fastest are the ones who have a clean data room before the term sheet arrives. At minimum, prepare:

- Audited or reviewed financial statements (or clean, well-organized books if pre-audit stage)

- Monthly P&L, cash flow, and balance sheet for the trailing 12-24 months

- MRR/ARR breakdown with cohort analysis

- Cap table with all outstanding instruments and conversion scenarios

- Corporate documents (certificate of incorporation, bylaws, board minutes)

- IP assignment agreements for all founders, employees, and contractors

- Key customer contracts

- Employee/contractor agreements

Financial readiness is a competitive advantage. When two comparable startups are raising at the same time, the one with clean books and an organized data room closes weeks faster. That speed matters. Market conditions change, competing term sheets expire, and investor enthusiasm fades.

How to Pitch to a VC

Everything above is context for this section. When you understand how VCs think, what they're optimizing for, and where you are in their process, pitching becomes strategic instead of performative.

Getting the Meeting

The warm introduction remains the single highest-leverage action in fundraising. Here's the priority order:

- Portfolio founder introductions. If you know someone the VC has already backed, ask them to make the intro. This is the gold standard.

- Other founder introductions. Founders who've interacted with the VC but didn't take money can still make warm intros.

- Investor network. Angels or other VCs who know the target partner.

- Cold outreach. Last resort, but can work if tightly targeted. Reference something specific the partner has written or invested in. Keep it to three sentences.

What the First Meeting Is Actually For

The first meeting is not a decision point. No one gets funded in a first meeting. The VC is doing three things:

Pattern matching. Does this fit our thesis? Is this founder credible? Is this market interesting?

Calibrating conviction. On a scale of "definitely not" to "I need to learn more," where does this fall?

Deciding whether to spend more time. That's it. Your goal isn't to close the deal. It's to earn the second meeting.

What Your Deck Needs to Do

Your deck is not a document. It's a conversation starter. The best decks do three things:

Establish the problem as real and urgent. Not theoretical. Show evidence that people are struggling with this problem today and spending money (or losing money) because of it.

Show that you've found something that works. Traction, early customers, a unique insight, something that demonstrates you're not just guessing.

Make the opportunity feel large and inevitable. The market is big. The timing is right. And you're positioned to win.

Keep it to 12-15 slides. Every additional slide dilutes your strongest points.

Handling Objections

Objections are buying signals. A VC who's not interested doesn't bother pushing back. They just smile and say "interesting" until the meeting ends.

When you get an objection:

Acknowledge it. "That's a fair concern" is better than getting defensive.

Address it with data. "Our churn was 8% monthly six months ago. We identified the root cause (onboarding friction) and it's now at 3.5% and still improving."

Reframe if appropriate. "The market looks small if you define it as X, but our customers are actually replacing Y, which is a $4B category."

What you should never do: argue, get defensive, dismiss the concern, or make promises you can't back up with evidence.

Follow-Up That Works

After every meeting, send a brief email within 24 hours. Thank them for their time. Address any open questions. Attach any materials they requested.

Then follow up every 1-2 weeks with genuine updates. Not "just checking in" emails. Share real progress: a new customer signed, a key hire made, a metric that moved. This demonstrates momentum and keeps you top of mind.

If they pass, ask for feedback and whether they'd reconsider at a future stage. Not every "no" is permanent. Some are "not yet."

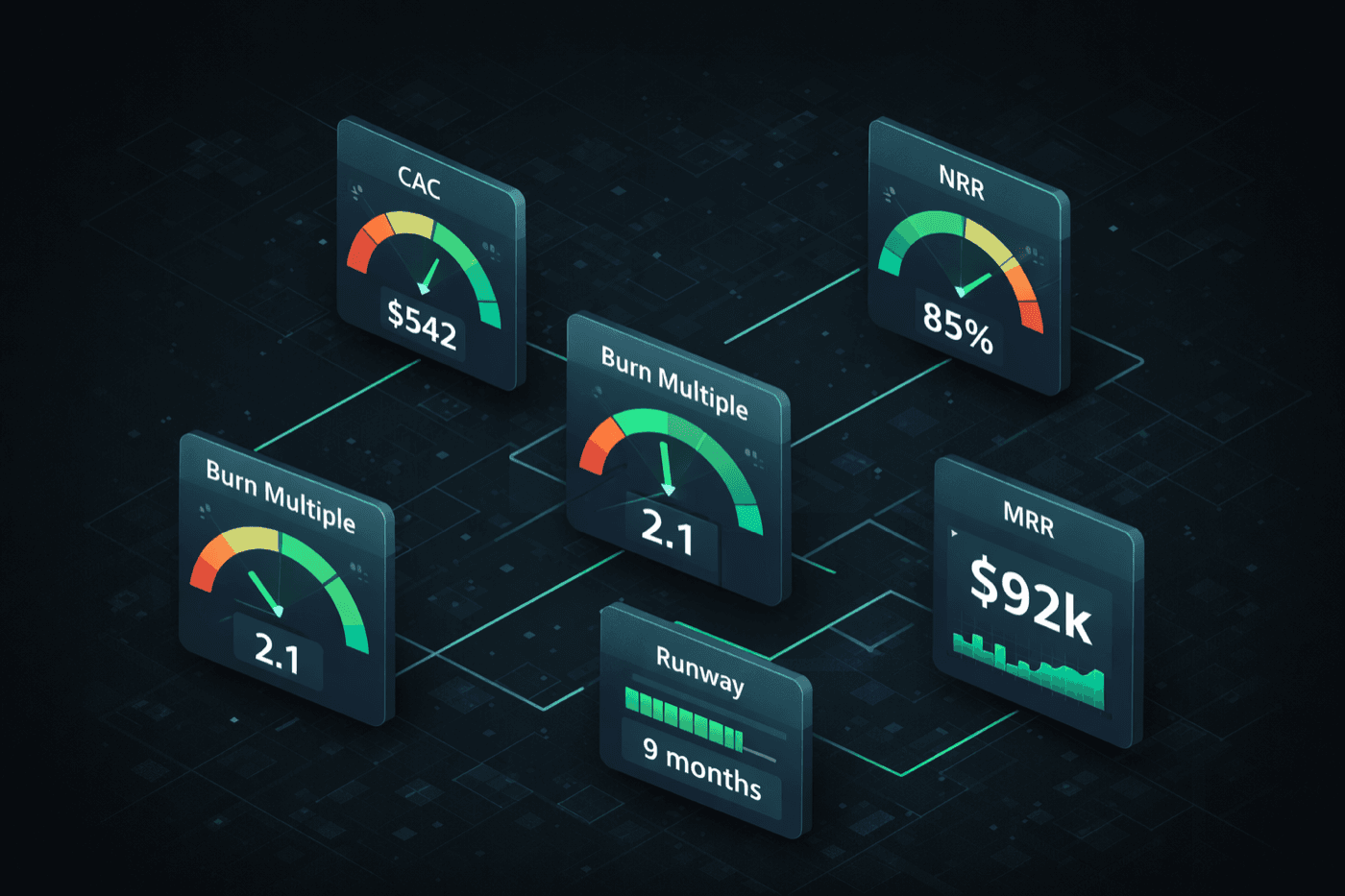

What Your Financials Need to Look Like Before You Raise

Everything in this guide funnels into one practical truth: VCs will look at your numbers. The question is whether those numbers help your case or hurt it.

At minimum, be ready to present:

- Profit and loss statement showing revenue, COGS, and operating expenses with clear line items

- Cash flow statement demonstrating how cash moves through the business

- Runway model showing months of cash remaining under current and projected burn

- MRR and ARR trends broken down by new, expansion, contraction, and churned revenue

- Burn multiple showing how efficiently you convert spend into growth

- Unit economics including CAC, LTV, LTV:CAC ratio, and payback period

Founders who walk into investor meetings with clean, credible financials move through diligence faster, negotiate from a position of strength, and close rounds while other founders are still scrambling to reconcile their books.

If your books are messy, your metrics are approximations, or you can't answer a basic question about your burn rate without checking a spreadsheet, fix that before you start fundraising. The cost of delay is far less than the cost of walking into a partner meeting unprepared.

Get your financials investor-ready with Futureproof →

The Bottom Line

Understanding how the venture capital process works won't guarantee you a yes. But it eliminates the avoidable nos: the ones caused by misreading the room, fumbling diligence, or pitching the wrong fund at the wrong time.

The things within your control (preparation, financial clarity, targeting the right investors, and managing the process with discipline) are the same things that separate funded founders from everyone else. VCs don't fund the best ideas. They fund the founders who make investing feel like a low-risk decision.

Do the work before the first meeting, and the process takes care of itself.

Not sure if you're ready? Our free Startup Fundraising Scorecard evaluates your readiness across 15 dimensions (team, market, traction, financial clarity, and fundraising preparedness) in 5 minutes.