The federal Research and Development (R&D) tax credit is one of the most valuable and underutilized tax benefits available to startups. Pre-revenue and early-revenue companies can apply the credit against payroll taxes (up to $500,000 per year), providing real cash savings during the stage when capital preservation matters most.

Despite this, many seed and Series A companies either do not know the credit exists or assume they do not qualify. Most software companies with engineering teams do qualify. This guide covers the eligibility requirements, qualified activities, calculation methodology, and documentation standards.

What the R&D Tax Credit Provides

The federal R&D tax credit (Section 41 of the Internal Revenue Code) offers two applications:

For profitable companies: A dollar-for-dollar reduction in federal income tax liability.

For pre-revenue or unprofitable startups (the PATH Act provision): A credit applied against employer payroll taxes instead of income tax, up to $500,000 per year for tax years beginning after 2022 (the Inflation Reduction Act doubled the original $250,000 limit). The first $250,000 offsets the employer's share of Social Security tax (6.2%); the second $250,000 offsets the employer's share of Medicare tax (1.45%). Companies can elect this for up to 5 tax years.

Eligibility for the payroll tax offset:

- Gross receipts below $5 million for the credit year

- No gross receipts for any tax year before the 5-tax-year period ending with the credit year

- In practical terms: startups less than 5 years old with under $5M in annual revenue

The Credit vs. the Deduction (Section 41 vs. Section 174)

Founders often conflate the Section 41 credit with Section 174 treatment of R&D expenses. They are separate things. Section 174 governs how R&D costs are deducted: from 2022 through 2024, domestic R&D costs had to be capitalized and amortized over five years, which created taxable income for startups that were losing money on a cash basis. Legislation in 2025 restored immediate expensing for domestic R&D, while foreign R&D still amortizes over 15 years. The Section 41 credit sits on top of that deduction treatment; claiming one does not replace the other, and if you filed during the capitalization era, ask your CPA how prior-year capitalized amounts unwind.

What Qualifies as R&D Activity

The IRS applies a four-part test. All four criteria must be met for an activity to qualify.

1. Permitted Purpose

The activity must relate to developing or improving a product, process, software, technique, formula, or invention. For software companies, this includes:

- Developing new features or functionality

- Building internal tools that solve technical challenges

- Designing system architecture

- Developing algorithms or data models

- Creating APIs and integrations

Does not qualify: Routine maintenance, bug fixes for known issues, quality assurance testing, UI changes without technical uncertainty, market research.

2. Technological Uncertainty

The activity must address uncertainty about the capability, method, or design of the product. The developer must not know in advance whether the approach will work or what the optimal solution is.

Qualifies: "Can we build a real-time reconciliation engine that processes 10,000 transactions per second?" The answer is not known at the outset.

Does not qualify: "Can we add a new button to the settings page?" There is no technical uncertainty.

3. Process of Experimentation

The activity must involve evaluating one or more alternatives through modeling, simulation, systematic trial and error, or other methods. In software development, iterative development with testing of different technical approaches typically satisfies this requirement.

4. Technological in Nature

The activity must rely on principles of engineering, computer science, biological science, or physical science. Software development inherently satisfies this criterion.

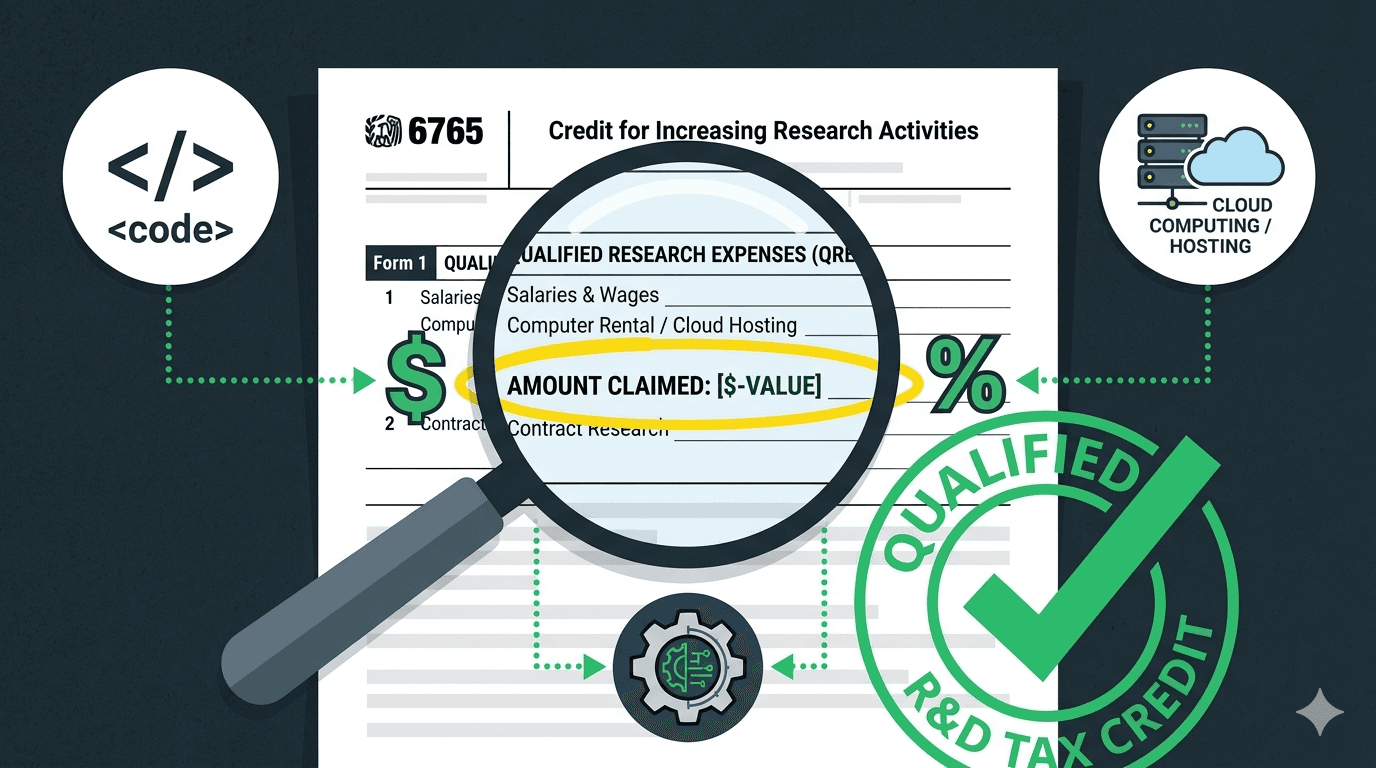

What Expenses Qualify

Qualified Research Expenses (QREs)

Wages and salaries: The portion of engineer, developer, and technical employee compensation attributable to qualifying R&D activities. This is typically the largest component, often 65-80% of the total credit. Only the time spent on qualifying activities counts. A developer who spends 70% of their time on qualifying work and 30% on maintenance contributes 70% of their salary as a QRE.

Contract research: 65% of payments to US-based contractors performing qualified research on behalf of the company. Note the 65% limitation: only two-thirds of contractor costs qualify.

Supplies: Materials consumed in the R&D process. For software companies, this bucket is usually small.

Rental or lease of computers: This is where cloud computing belongs. Cloud costs used for development and testing environments (not production infrastructure) qualify as payments for the rental or lease of computers, not as supplies. Same dollars, but your documentation should use the right label.

What Does Not Qualify

- Sales and marketing expenses

- Administrative overhead

- Production infrastructure costs (hosting for customers)

- Training costs

- Market research and customer discovery

- Management time unless directly contributing to technical research

How to Calculate the Credit

Two calculation methods are available. Most startups use the simplified method.

Alternative Simplified Credit (ASC) Method

This is the most common method for startups.

Step 1: Calculate total QREs for the current year.

- Engineering salaries attributable to R&D: $420,000

- Contract developers (65% of total): $58,500

- Cloud development costs: $12,000

- Total QREs: $490,500

Step 2: Calculate the base amount. Average QREs from the prior 3 years × 50%.

- Year 1 QREs: $280,000

- Year 2 QREs: $350,000

- Year 3 QREs: $400,000

- Average: $343,333

- Base amount: $343,333 × 50% = $171,667

Step 3: Calculate the credit. (Current QREs - Base Amount) × 14%

- Credit = ($490,500 - $171,667) × 14% = $44,637

For first-year claimants with no prior QRE history, a simplified approach uses 6% of current-year QREs:

- First-year credit = $490,500 × 6% = $29,430

Applying the Credit Against Payroll Taxes

For eligible startups, file Form 6765 with your annual tax return and Form 8974 with your quarterly payroll tax filing (Form 941). The first $250,000 of credit each year offsets the employer's 6.2% Social Security tax; amounts above that, up to the second $250,000, offset the employer's 1.45% Medicare tax.

Using the example above: a $44,637 credit saves $44,637 in quarterly payroll tax payments, real cash back in the company's bank account. The offset applies quarter by quarter against your actual payroll tax liability, starting the first quarter after the return claiming the credit is filed, with unused amounts carrying forward to later quarters. It is not a lump-sum refund.

One procedural point matters: the payroll-offset election must be made on an original, timely filed return. You cannot amend your way into it later.

Documentation Requirements

The IRS requires contemporaneous documentation. Building the habit of documentation from day one significantly reduces the cost and effort of claiming the credit.

What to Document

Time tracking: Record how engineers allocate time between qualifying R&D activities and non-qualifying work. This can be as simple as project-level tracking in your project management tool (Jira, Linear, Asana) with tags for R&D qualification.

Project descriptions: For each qualifying project, document:

- The technical uncertainty being addressed

- The alternatives considered or tested

- The process of experimentation followed

- The outcome and technical learnings

Expense allocation: Map expenses to specific R&D projects. Maintain records of which employees worked on qualifying projects and the percentage of time allocated.

Technical records: Commit histories, design documents, architecture decisions, and testing results all serve as supporting documentation.

Documentation Best Practices

- Track at the project level, not the individual task level

- Tag R&D-qualifying projects in your project management system

- Have engineering leads review time allocations quarterly

- Store documentation in a dedicated folder accessible to your tax preparer

- Do not create documentation retroactively. Contemporaneous records carry more weight

State R&D Tax Credits

In addition to the federal credit, many states offer their own R&D tax credits. States with significant credits include California, Massachusetts, New York, Texas, Georgia, and Connecticut. State credits can add 5-20% on top of the federal benefit.

Consult a tax advisor for state-specific requirements, as each state has different qualification criteria and calculation methods.

Working with a Tax Professional

While this guide covers the framework, R&D tax credit claims should be prepared or reviewed by a qualified tax professional. The cost of professional preparation (typically $3,000-$10,000 for a startup-sized claim) is generally well below the credit value.

When selecting a provider, evaluate:

- Experience with software company R&D credits specifically

- Willingness to support the claim in the event of an IRS review

- Whether they perform a technical assessment or rely only on financial data

- Fee structure (fixed fee is preferable to a percentage of the credit)

The Role of Clean Bookkeeping

Accurate R&D tax credit claims depend on properly categorized expenses. If engineering salaries are lumped together with other payroll, or if contractor payments are not separated from other vendor costs, the documentation required for the credit becomes significantly more difficult.

Futureproof helps SaaS startups maintain properly categorized expenses from day one, separating engineering costs, contractor payments, and infrastructure expenses into the right accounts. This makes R&D credit claims faster, more accurate, and less expensive to prepare.

Key Takeaway

The R&D tax credit provides meaningful cash savings ($30,000 to $500,000 annually) for startup companies that are developing software. The qualifying criteria are broad enough that most engineering teams performing product development will meet them. The primary barriers are awareness and documentation discipline, not eligibility.

Start documenting qualifying activities now, even if you are not ready to file a claim. Retroactive documentation is more expensive and less defensible than real-time records.