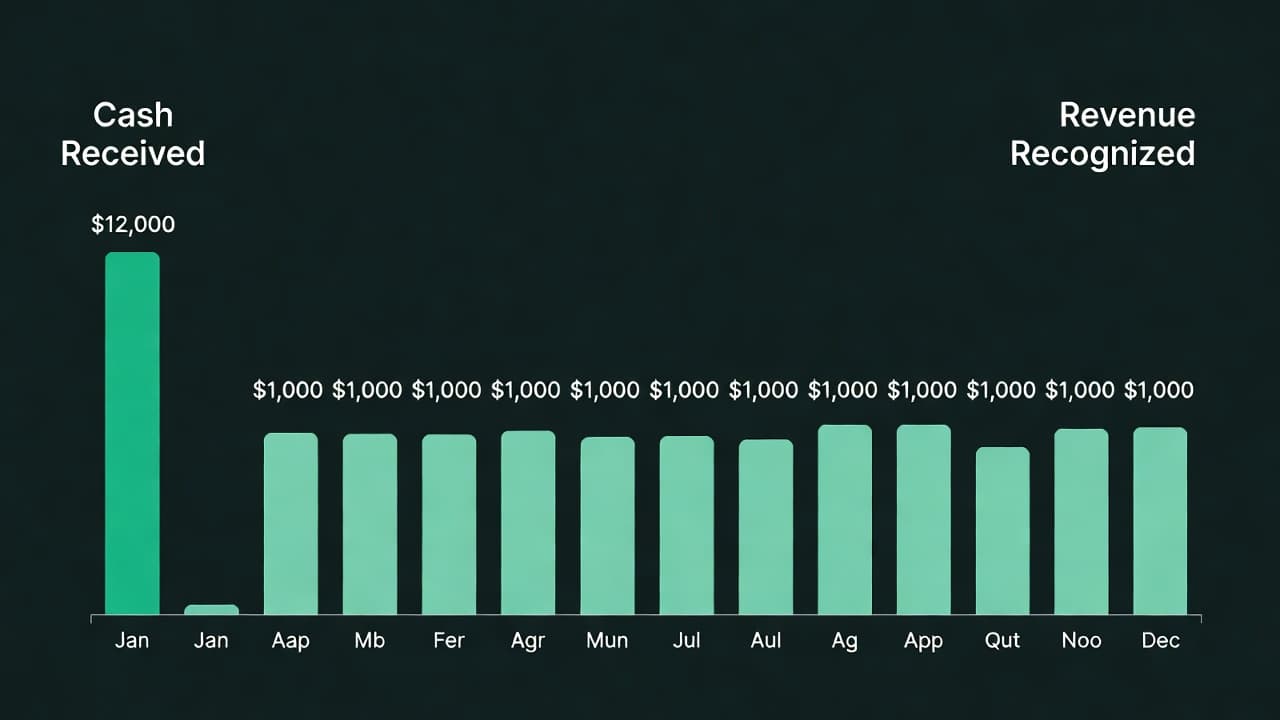

A SaaS company collects $120,000 in annual prepayments on January 1. The cash is in the bank. But on the income statement, the company can only recognize $10,000 of revenue in January. The remaining $110,000 sits on the balance sheet as a liability called deferred revenue.

This creates a counterintuitive situation: a company's bank account shows $120,000, but its income statement shows only $10,000 in revenue. Understanding this distinction is fundamental to SaaS financial management, and one of the most common areas where early-stage founders make errors.

What Deferred Revenue Is

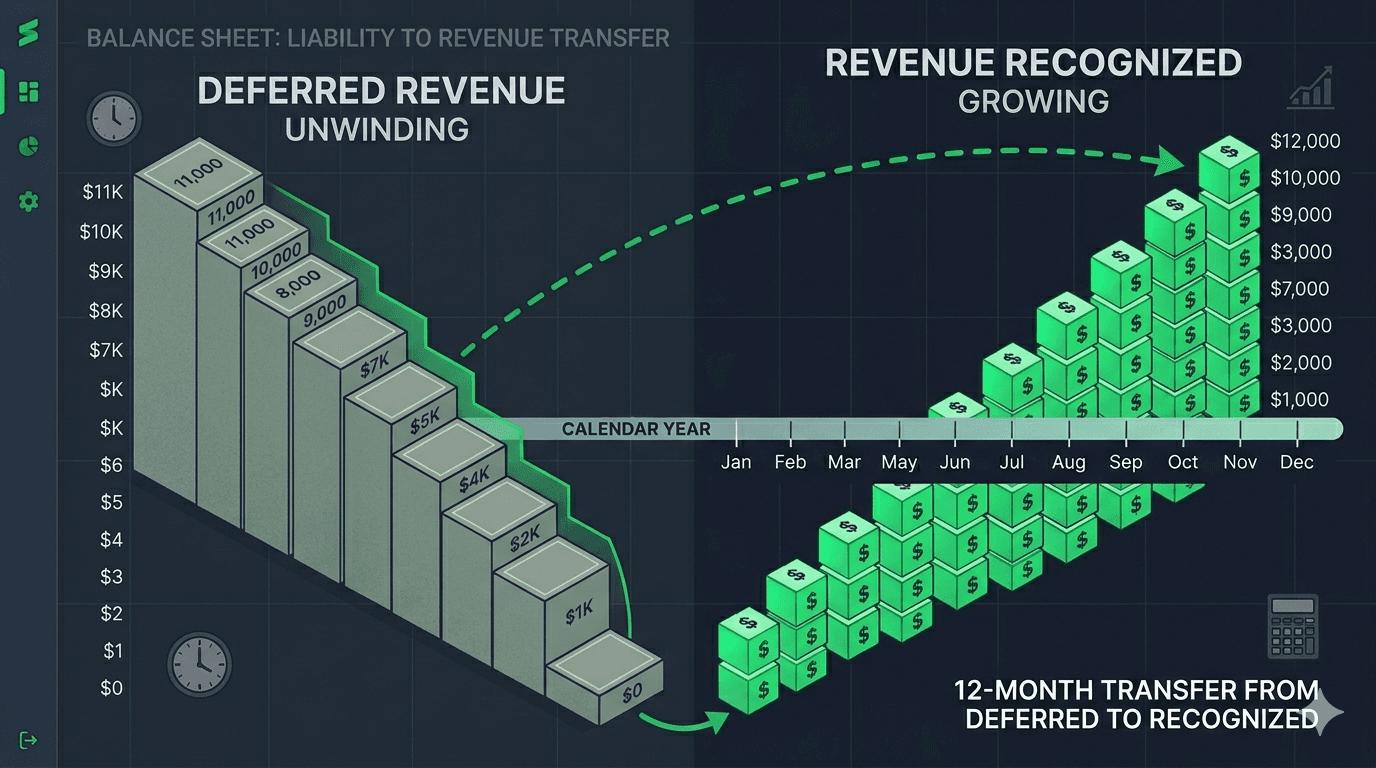

Deferred revenue (also called unearned revenue) represents payments received for services that have not yet been delivered. It is classified as a current liability on the balance sheet because the company owes the customer future service delivery. On multi-year prepayments, only the portion that will be earned within the next 12 months belongs in current liabilities; anything beyond that is classified as long-term deferred revenue.

The "liability" framing often confuses founders. The company does not owe the customer cash. It owes them service. As the service is delivered month by month, deferred revenue decreases and recognized revenue increases. No cash changes hands during this process; it is purely an accounting adjustment.

How Deferred Revenue Works in Practice

The Monthly Mechanics

A customer signs a 12-month contract at $2,400/year, paid upfront on March 1.

On March 1 (payment date):

- Cash increases by $2,400

- Deferred revenue increases by $2,400

- Revenue recognized: $0

On March 31 (end of first month):

- Deferred revenue decreases by $200

- Revenue recognized: $200

This repeats each month until February 28 of the following year:

- Deferred revenue reaches $0

- Total revenue recognized: $2,400

At Scale

A SaaS company with 200 annual customers paying $3,600/year has:

- Annual cash collected: $720,000

- Average deferred revenue balance: ~$360,000 (half of annual prepayments, assuming even distribution of contract start dates)

- Monthly revenue recognized: $60,000

The deferred revenue balance represents approximately 6 months of future revenue that has already been collected but not yet earned.

Why Deferred Revenue Matters

For Cash Flow Management

Deferred revenue creates a timing advantage. Annual prepayments provide cash that funds operations months before the corresponding revenue is recognized. This is one reason SaaS companies with annual billing have stronger cash flow than those billing monthly. The customer finances months of operations in advance.

However, this advantage creates a dependency. If annual prepayment rates decline (customers switching to monthly billing), cash flow drops even if revenue metrics remain stable.

For Financial Statement Accuracy

Deferred revenue directly affects three financial statements:

Balance Sheet: Appears as a current liability, increasing total liabilities and reducing working capital and current ratio. For SaaS companies, adjusting these ratios to exclude deferred revenue provides a more operationally accurate picture.

Income Statement: Revenue flows from deferred revenue to the income statement as service is delivered. Incorrect recognition timing distorts gross margin, operating margin, and profitability metrics.

Cash Flow Statement: Cash from annual prepayments flows through the operating cash flow section. A growing deferred revenue balance increases operating cash flow even if the company is recognizing less revenue. This is not a sign of operational improvement, it reflects timing.

For Investor Evaluation

Investors evaluate deferred revenue in several ways:

Growing deferred revenue is positive. It indicates increasing forward commitments and customer willingness to prepay. A deferred revenue balance growing faster than recognized revenue suggests strong sales of annual contracts.

Declining deferred revenue is a warning. It may indicate that new bookings are slowing, customers are shifting from annual to monthly billing, or churned contracts are not being replaced at renewal.

Deferred revenue adjustments to metrics. Sophisticated investors adjust current ratio and working capital to exclude deferred revenue, recognizing that it represents committed service obligations rather than cash that might need to be returned.

Billings is the growth signal investors compute from this balance. Billings equals recognized revenue plus the change in deferred revenue for the period. It approximates what was invoiced to customers, and because recognized revenue lags sales by design, billings is often the better read on current sales momentum.

Common Deferred Revenue Mistakes

1. Recognizing Prepaid Revenue Immediately

The most frequent error. Recognizing a $24,000 annual payment as $24,000 of revenue in the collection month overstates current-period revenue and leaves no deferred revenue on the balance sheet. This creates mismatched financial statements that will need correction before any investor due diligence.

2. Not Tracking Deferred Revenue at All

Some early-stage companies operate on a cash basis and do not maintain deferred revenue schedules. This works until a potential investor, acquirer, or auditor asks for accrual-based financial statements, at which point retroactive reconstruction is expensive and error-prone.

3. Inconsistent Treatment Across Contract Types

Applying different recognition methods to similar contracts (e.g., deferring annual contracts but immediately recognizing quarterly contracts) creates inconsistency that is flagged during audits.

4. Confusing Deferred Revenue with Deposits

Customer deposits for future work (e.g., a retainer) are similar to deferred revenue but may have different accounting treatment depending on the terms. Ensure proper classification.

5. Ignoring the Balance Sheet Impact on Ratios

A SaaS company with $500K in current assets and $400K in current liabilities reports a current ratio of 1.25, which appears weak. But if $250K of those liabilities is deferred revenue that will be earned by delivering service (not returned as cash), the adjusted ratio is 3.33. Both the company and its investors should understand this distinction.

How to Set Up Deferred Revenue Tracking

Manual Approach (Spreadsheet)

Create a deferred revenue schedule with columns for:

- Customer name

- Contract start date

- Contract end date

- Total contract value

- Monthly recognition amount

- Remaining deferred balance

Update monthly by recognizing the appropriate amount and reducing the deferred balance. This approach works for companies with fewer than 50 annual contracts.

Accounting Software Configuration

Both QuickBooks and Xero support deferred revenue through journal entries:

- On payment receipt: Debit Cash, Credit Deferred Revenue (liability)

- Monthly: Debit Deferred Revenue, Credit Revenue

Configure recurring journal entries for each annual or multi-year contract to automate the monthly recognition.

Automated Platform

Futureproof automates deferred revenue accounting for SaaS companies by connecting to Stripe and billing systems. Annual and multi-year contracts are automatically deferred and recognized on the correct schedule, ensuring the balance sheet, income statement, and SaaS metrics remain consistent without manual journal entries.

Deferred Revenue and SaaS Metrics

Deferred revenue affects how several key metrics should be calculated and interpreted:

- MRR: Should be based on recognized recurring revenue, not collected cash

- ARR: Same. Use the recognized monthly run rate, not annualized collections

- Gross Margin: Revenue in the margin calculation should be recognized revenue

- Cash Flow vs Revenue: These will diverge for companies with significant annual prepayments. Both numbers are important and serve different purposes

The core principle: revenue recognition and cash collection are separate processes. Treating them as equivalent produces inaccurate financial statements and misleading metrics.