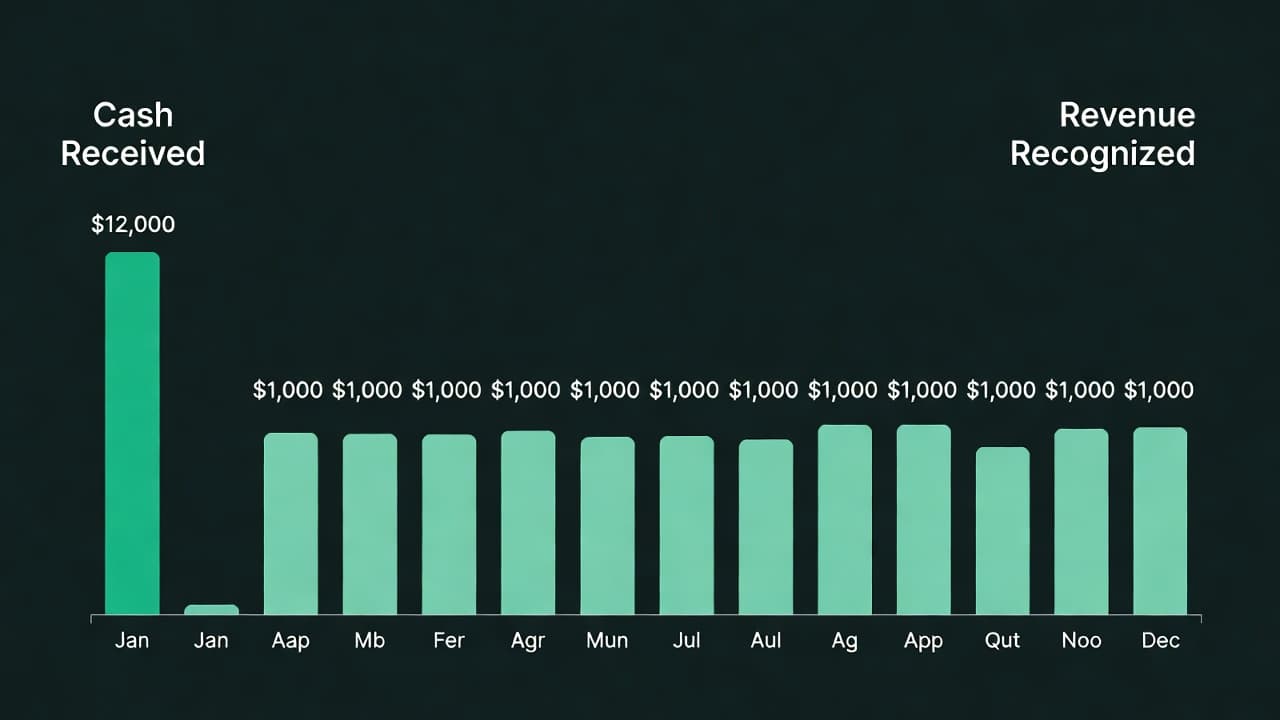

Revenue recognition is one of the most misunderstood areas of SaaS accounting. A customer pays $12,000 upfront for an annual subscription. The cash hits your bank account on day one, but you cannot recognize the full $12,000 as revenue immediately. Under ASC 606, that $12,000 is recognized at $1,000 per month as the service is delivered.

This distinction between cash received and revenue recognized affects everything: your income statement, balance sheet, ARR calculations, gross margin, and how investors evaluate your business. Getting it wrong creates problems that compound over time, and they often surface at the worst possible moment, during a fundraise or acquisition.

Why Revenue Recognition Matters for SaaS Founders

For fundraising: Investors and their accountants will scrutinize your revenue recognition practices during due diligence. Improperly recognized revenue, even if unintentional, erodes credibility and can delay or kill a round.

For metrics accuracy: MRR and ARR are based on recognized recurring revenue, not cash collected. Conflating the two produces inaccurate metrics that lead to flawed decisions.

For financial statements: Revenue recognition determines deferred revenue balances on your balance sheet, which affects working capital, current ratio, and other financial health indicators.

The ASC 606 Five-Step Framework

ASC 606 (Accounting Standards Codification Topic 606) establishes a five-step model for recognizing revenue. For most SaaS companies, the application is straightforward.

Step 1: Identify the Contract

A contract exists when both parties agree to terms, each party's rights and payment terms are identified, and the arrangement has commercial substance. For SaaS, this is typically the signed subscription agreement or accepted terms of service.

Step 2: Identify Performance Obligations

A performance obligation is a promise to deliver a distinct good or service. In SaaS, the primary performance obligation is providing access to the software platform over the subscription period.

Common SaaS performance obligations:

- Software access (the subscription itself)

- Implementation or onboarding services

- Customer support

- Training or consulting hours

- Data migration

Each distinct obligation must be evaluated separately. If implementation is sold as a separate line item and has standalone value, it is a separate performance obligation with its own recognition timeline.

Step 3: Determine the Transaction Price

The total consideration the company expects to receive. For straightforward SaaS subscriptions, this is the contract price. For contracts with variable components (usage-based pricing, discounts, credits), the transaction price requires estimation.

Step 4: Allocate the Price to Performance Obligations

If a contract includes multiple performance obligations, allocate the total price based on each obligation's relative standalone selling price. If the bundle is sold at a discount, the discount is spread proportionally across the obligations rather than assigned to any single one.

Example: A $15,000 annual contract includes $12,000 for software access and $3,000 for implementation.

- Software: Recognized ratably over 12 months ($1,000/month)

- Implementation: Recognized when the service is delivered (upon completion)

Step 5: Recognize Revenue as Obligations Are Satisfied

Revenue is recognized when (or as) each performance obligation is satisfied.

- Over time (ratably): Software subscriptions. Revenue is recognized evenly over the subscription period because the customer receives value continuously.

- At a point in time: Implementation, training, or one-time deliverables. Revenue is recognized when the service is complete.

Common SaaS Revenue Recognition Scenarios

Monthly Subscriptions

The simplest case. Revenue is recognized in the month the service is provided. Cash collection and revenue recognition typically align.

- Customer pays $500 on March 1 for March access

- Revenue recognized: $500 in March

Annual Subscriptions (Prepaid)

Cash is received upfront but revenue is recognized monthly.

- Customer pays $6,000 on January 1 for 12 months of access

- Revenue recognized: $500 per month, January through December

- Deferred revenue on January 1, when payment is received: $6,000, because nothing has been delivered yet

- After January's $500 is recognized, the balance drops to $5,500 (the 11 months not yet delivered), then decreases by $500 each month

Multi-Year Contracts

Revenue is recognized ratably over the full contract term.

- Customer signs a 3-year, $90,000 contract

- Revenue recognized: $2,500 per month for 36 months

- Initial deferred revenue: $90,000 if the full contract is prepaid, dropping to $87,500 after the first month's recognition

In practice, most 3-year deals bill annually rather than all upfront, in which case only the invoiced year sits in deferred revenue at any given time.

Contracts with Setup Fees

Setup or implementation fees are evaluated for standalone value.

- If the setup service has standalone value (the customer could hire another vendor to do it): Recognize setup revenue when complete, subscription revenue ratably

- If the setup has no standalone value (it only makes sense in the context of the subscription): Combine with the subscription and recognize the total ratably over the contract term

- One nuance: if a non-refundable upfront fee means renewing customers avoid paying it again, that discount is a material right, and the fee may need to be recognized over the expected customer life rather than just the initial term

Usage-Based Components

Variable pricing tied to API calls, transactions, or data volume. Revenue is recognized as usage occurs, typically monthly based on actual consumption. Where usage must be estimated, ASC 606's variable-consideration constraint applies: include estimated amounts only to the extent a significant revenue reversal is not probable.

Free Trials

No revenue is recognized during the trial period. Revenue recognition begins when the trial converts to a paid subscription.

Sales Commissions (ASC 340-40)

Revenue recognition has a companion standard that founders often miss. Under ASC 340-40, sales commissions paid to win new contracts are capitalized as an asset and amortized over the expected period of benefit, often the anticipated customer life rather than just the initial contract term, instead of being expensed when paid. Every Series A diligence process checks for this, so establish a commission capitalization schedule alongside your revenue recognition policy.

Deferred Revenue: The Balance Sheet Impact

Deferred revenue (also called unearned revenue) represents cash received for services not yet delivered. It is a liability on the balance sheet because the company owes the customer future service.

Why it matters for SaaS companies:

- A growing SaaS company with annual prepayments will have a large deferred revenue balance. This is healthy. It indicates strong forward commitments.

- Deferred revenue affects current ratio and working capital calculations. For SaaS companies, adjusting these metrics to account for deferred revenue provides a more accurate picture of financial health.

- Investors view growing deferred revenue positively. It represents contractually committed future revenue.

Example balance sheet impact:

A company collects $240,000 in annual prepayments on January 1.

| Month | Revenue Recognized | Deferred Revenue Balance |

|---|---|---|

| January | $20,000 | $220,000 |

| February | $20,000 | $200,000 |

| March | $20,000 | $180,000 |

| ... | ... | ... |

| December | $20,000 | $0 |

Common Revenue Recognition Mistakes

1. Recognizing annual contract revenue upfront The most common error. An annual prepayment of $24,000 is not $24,000 in revenue on the collection date. It is $2,000/month recognized over 12 months. This mistake inflates current-period revenue and creates problems during audit or due diligence.

2. Not separating performance obligations A $30,000 contract that includes $24,000 for software and $6,000 for implementation should not be recognized as $2,500/month for 12 months. The implementation revenue should be recognized separately when delivered.

3. Recognizing revenue before delivery begins If a customer prepays for a subscription starting next quarter, no revenue is recognized until the service period begins. The entire amount sits in deferred revenue until the start date.

4. Inconsistent treatment across customers Applying different recognition methods to similar contracts creates audit risk. Establish a revenue recognition policy and apply it consistently.

5. Confusing bookings with revenue Bookings represent the total value of signed contracts. Revenue represents the amount recognized under ASC 606. These are distinct metrics and should be tracked separately.

Implementing Proper Revenue Recognition

For Early-Stage Companies (Pre-Seed to Seed)

- Set up separate revenue accounts for recurring and non-recurring revenue

- Configure your accounting software to automatically defer annual prepayments

- Create a simple revenue recognition schedule in a spreadsheet

- Document your revenue recognition policy (even a one-page document)

For Growth-Stage Companies (Seed to Series A)

- Ensure your chart of accounts properly separates revenue streams

- Implement automated deferred revenue calculations in your accounting system

- Have your accountant or auditor review your recognition practices before fundraising

- Align revenue recognition with MRR and ARR calculations

Automated Approach

Futureproof handles revenue recognition automatically for SaaS subscription revenue, deferring annual prepayments, recognizing monthly amounts, and maintaining accurate deferred revenue balances without manual spreadsheet tracking. This ensures your financial statements, metrics, and board reports are always consistent and audit-ready.

Key Takeaway

Revenue recognition is not optional or negotiable. ASC 606 establishes the standard, and adherence becomes increasingly important as a company grows toward institutional fundraising. Establishing proper practices early, even at the seed stage, prevents the costly corrections that surface during due diligence.

The fundamental rule: recognize revenue when the service is delivered, not when the cash is received. Everything else follows from that principle.