Most startup accounting advice presents accrual and cash basis accounting as an either/or decision. In practice, SaaS and ecommerce companies need both: accrual for operational decision-making and investor reporting, cash basis for tax optimization. Running on only one creates blind spots that cost money.

This guide covers why each method exists, when to use which, the mechanics of maintaining both, and how automated revenue recognition eliminates the manual burden of dual-basis accounting.

The Two Methods, Briefly

Cash basis accounting records revenue when cash is received and expenses when cash is paid. It tracks what actually happened in your bank account.

Accrual accounting records revenue when earned and expenses when incurred, regardless of when cash moves. It tracks economic activity as it happens.

The difference is timing. Over the life of a business, both methods produce the same total revenue and expenses. But in any given month or quarter, they can tell dramatically different stories.

Why the Difference Matters: A SaaS Example

A SaaS company signs three annual contracts on January 1, each at $24,000/year prepaid.

Cash basis view of January:

| Amount | |

|---|---|

| Revenue | $72,000 |

| Expenses | $35,000 |

| Profit | $37,000 |

Accrual basis view of January:

| Amount | |

|---|---|

| Revenue | $6,000 ($72K ÷ 12 months) |

| Expenses | $35,000 |

| Loss | -$29,000 |

Same company, same month. Cash basis says highly profitable. Accrual says burning cash. Neither is wrong. They answer different questions.

- Cash basis answers: "How much money moved this month?"

- Accrual answers: "How much economic value was created this month?"

For operational decisions (hiring, spending, forecasting), accrual gives the accurate picture. For tax purposes, cash basis often provides a significant advantage.

Why Ecommerce Has the Same Problem

An ecommerce company orders $80,000 in inventory in November, sells $120,000 of product in December, and pays the supplier in January.

Cash basis view of December:

| Amount | |

|---|---|

| Revenue | $120,000 (customer payments received) |

| COGS | $0 (supplier not yet paid) |

| Profit | $120,000 |

Accrual basis view of December:

| Amount | |

|---|---|

| Revenue | $120,000 |

| COGS | $60,000 (cost of goods actually sold) |

| Profit | $60,000 |

(This assumes 75% of the purchased units sold in December: $60,000 of the $80,000 inventory cost matches December's sales, and the remaining $20,000 stays on the balance sheet as inventory.)

Cash basis overstates December profit by $60,000 because the inventory cost hasn't been paid yet. January will show a massive expense hit for product already sold. Accrual correctly matches the cost to the revenue it generated.

For inventory management, pricing decisions, and gross margin analysis, accrual is essential. Cash basis makes it impossible to know your true COGS or contribution margin in real time.

Why SaaS and Ecommerce Need Accrual for Operations

1. Accurate SaaS Metrics Require Accrual

Every core SaaS metric depends on accrual-basis revenue recognition:

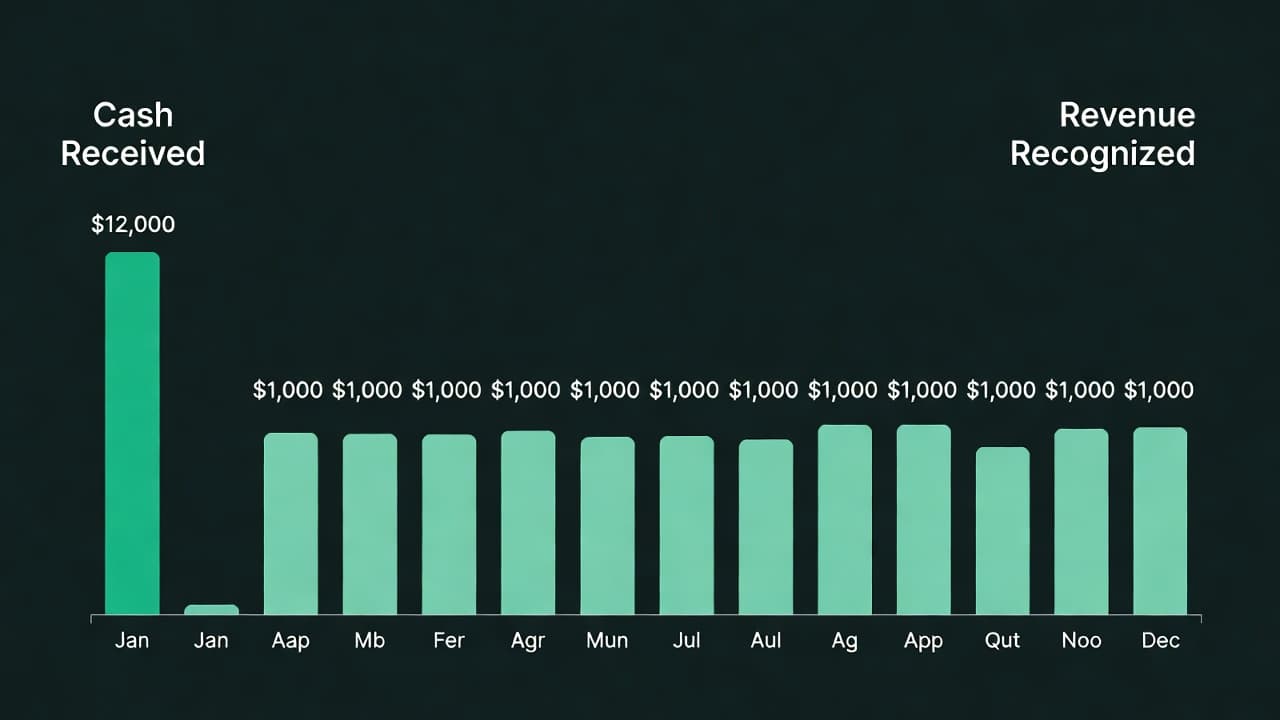

- MRR: Must reflect recognized monthly revenue, not collected cash. An annual prepayment of $12,000 contributes $1,000/mo to MRR, not $12,000 in the collection month.

- ARR: Same principle, annualized recognized revenue.

- Gross margin: Requires matching revenue to the costs incurred in delivering it during the same period.

- Net revenue retention: Tracks revenue changes from existing customers over time. Only meaningful on an accrual basis.

- Burn rate: While burn rate is often tracked on a cash basis (actual bank balance changes), the underlying expense recognition should be accrual-based for accurate trend analysis.

Running SaaS metrics on cash-basis numbers produces misleading results. A company that shifts from monthly to annual billing would show a massive revenue spike on cash basis, but nothing changed operationally.

2. Investor and Board Reporting Requires Accrual

Investors expect accrual-basis financial statements. GAAP (Generally Accepted Accounting Principles) requires accrual accounting. During due diligence for a Series A raise, presenting cash-basis financials signals either inexperience or an attempt to obscure the real economics.

Board reports built on cash-basis numbers create confusion. A quarter where several annual contracts renew will show inflated revenue, while a quarter without renewals will look flat, even if the underlying business is growing steadily.

3. Revenue Recognition Is an Accrual Concept

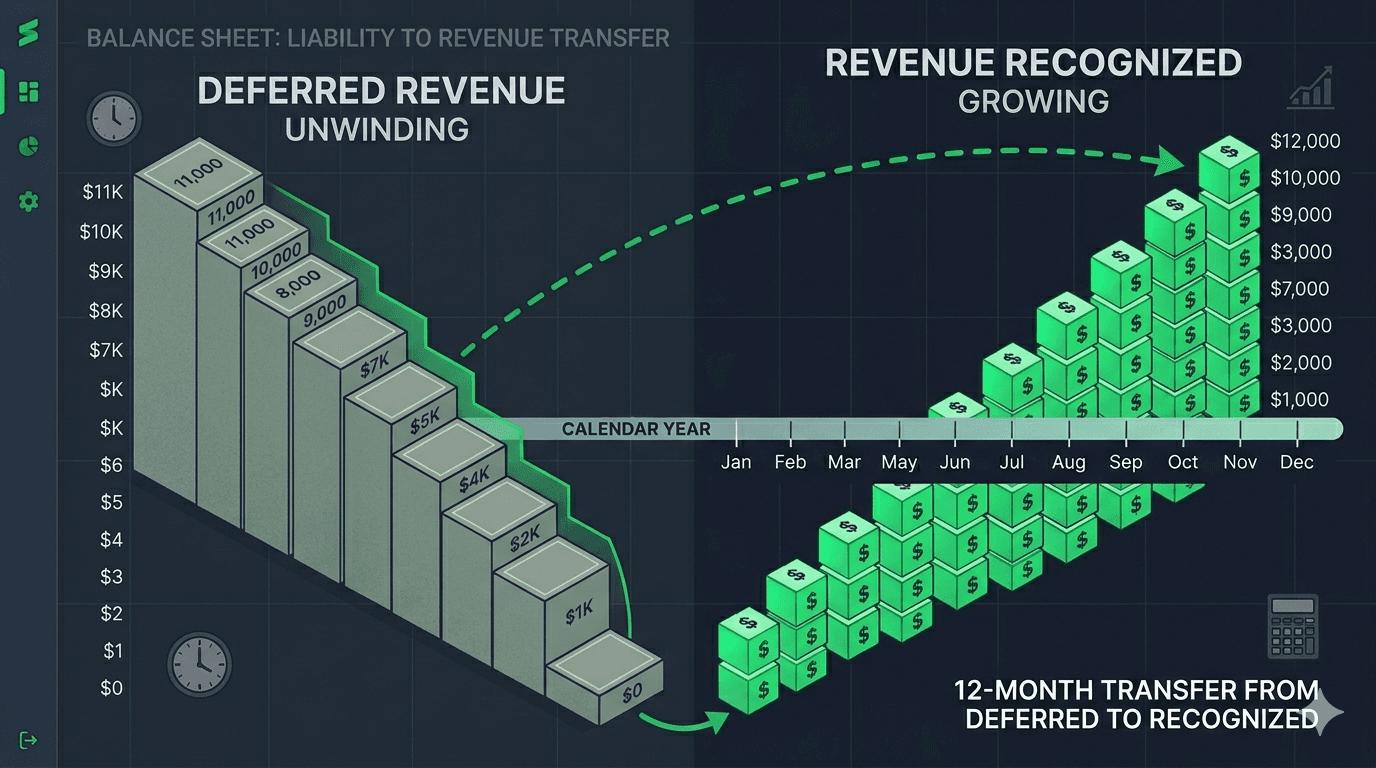

ASC 606 requires revenue to be recognized when the performance obligation is satisfied, when the service is delivered, not when payment is received. This is fundamentally an accrual concept. SaaS companies that collect annual prepayments must maintain deferred revenue schedules and recognize revenue ratably over the service period.

4. Ecommerce Inventory Accounting Requires Accrual

Matching COGS to the period in which goods are sold is an accrual principle. Cash-basis inventory accounting creates timing mismatches that make it impossible to calculate accurate gross margin, contribution margin, or break-even point in any given period.

Why Cash Basis Is Often Better for Taxes

Despite accrual's operational advantages, many startups file taxes on a cash basis. The IRS allows cash-basis reporting for companies with average annual gross receipts under roughly $31 million (the Section 448(c) threshold, expanded by the Tax Cuts and Jobs Act and indexed annually for inflation). Strictly speaking, the Section 448 limit binds C corporations and partnerships with a C corporation partner (tax shelters are barred from cash basis regardless of size); S corporations and most LLCs are not subject to Section 448 itself, though inventory and Section 471 rules still apply to them.

The Tax Advantage

Cash basis allows companies to defer taxable income by timing cash flows strategically:

Accelerate expenses: Pay Q1 vendor invoices in December. Prepay annual software subscriptions before year-end. Make equipment purchases before December 31. Under cash basis, these payments reduce current-year taxable income.

Defer revenue: Invoice customers in early January rather than late December so payment arrives in the new year. (Note the limit here: under the constructive receipt doctrine, a check received December 28 is December income even if you deposit it in January. The timing lever is when you bill, not when you deposit.)

Annual prepayments become immediate deductions: A $24,000 annual software contract paid in December is a $24,000 expense in the current tax year under cash basis. Under accrual, only 1/12 ($2,000) would be expensed in December.

The important exception: prepaid annual SaaS revenue cuts the other way. If your customers prepay annually, cash basis taxes the full December prepayment in the year you receive it. An accrual-method taxpayer, by contrast, can generally defer advance payments one year under Section 451(c), recognizing for tax only what is earned in year one and pushing the rest into the following year. For SaaS companies collecting significant annual prepayments, accrual can actually be the tax-favorable method. Model both with your CPA before assuming cash basis wins.

For a pre-profit SaaS company, the difference is often minimal (no taxable income to offset). But for profitable companies or those with significant R&D tax credit calculations, the method choice can save thousands in annual tax liability.

When Cash Basis Isn't Available for Taxes

Companies that exceed the roughly $31 million average annual gross receipts threshold must use accrual for tax purposes. Companies with inventory may have additional restrictions, though the TCJA relaxed these rules for smaller businesses. Even on cash basis, inventory generally cannot be deducted when paid for: it is treated as non-incidental materials and supplies, deductible as the items are sold or used. Consult a CPA for your specific situation.

How to Maintain Both: The Dual-Basis Approach

The standard practice for SaaS and ecommerce companies is:

- Primary books: Accrual basis for day-to-day operations, metrics, investor reporting, and board decks

- Tax filing: Cash basis converted from accrual at year-end by your CPA

The Manual Process (What Most Companies Do)

Step 1: Maintain accrual-basis books throughout the year. Record deferred revenue, accrued expenses, prepaid expenses, and accounts receivable / payable as they occur.

Step 2: At year-end, your CPA converts accrual to cash for the tax return. This involves a series of adjustments:

- Remove deferred revenue (add back cash collected but not yet recognized)

- Remove accrued expenses (remove expenses recorded but not yet paid)

- Remove prepaid expenses (add back cash paid for future periods)

- Adjust accounts receivable (remove revenue recognized but not yet collected)

- Adjust accounts payable (remove expenses incurred but not yet paid)

Step 3: File the tax return on cash basis.

Step 4: Continue operating on accrual basis in the new year.

The Problem with Manual Conversion

The year-end accrual-to-cash conversion is where errors compound. A company with 200 annual SaaS subscriptions starting on different dates has 200 deferred revenue schedules that must be correctly reversed. Prepaid expenses, accrued liabilities, and receivables must all be adjusted.

For most seed-stage companies, this conversion takes 10-20 hours of CPA time annually, costing $2,000-$5,000. Errors in the conversion create discrepancies between operational books and tax filings that surface during audits or due diligence.

How Futureproof Automates This

Futureproof eliminates the manual burden of dual-basis accounting by automating the most time-consuming components:

Automated Revenue Recognition

When a customer pays $12,000 annually via Stripe, Futureproof automatically:

- Records the $12,000 cash receipt

- Creates a $12,000 deferred revenue liability

- Recognizes $1,000/mo as earned revenue over 12 months

- Reduces the deferred revenue balance monthly

- Keeps the books clean and current on an accrual basis, so your CPA has accurate records at tax time

No manual journal entries. No spreadsheet-based deferred revenue schedules. No month-end reconciliation between what Stripe collected and what should be recognized.

Accrual Books Your CPA Can Work From

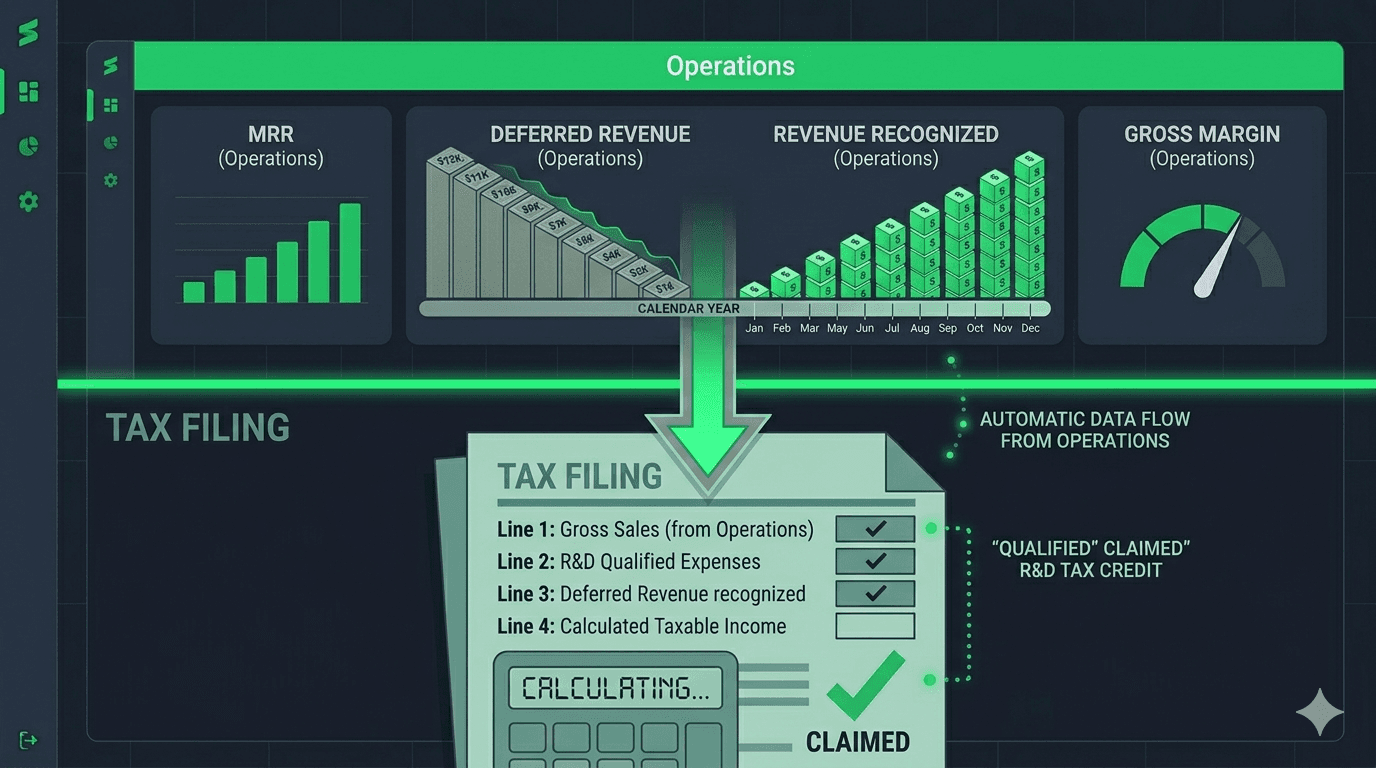

Futureproof maintains your books on an accrual basis, continuously:

- Accrual-basis financials for your dashboard, metrics, and investor reporting. MRR, ARR, gross margin, and burn rate are always accurate and current

- Clean records for tax preparation. Your CPA gets complete, current accrual books, with deferred revenue, prepaids, and accruals already tracked, to prepare whichever tax basis applies to your return

That turns the year-end conversion into a review exercise instead of a reconstruction project.

Automated Expense Matching

Prepaid expenses (annual software contracts, insurance premiums) are automatically amortized over the service period on accrual basis while remaining fully expensed on cash basis. Accrued expenses are tracked and reversed appropriately in each view.

Why Bookkeepers and Fractional CFOs Prefer This

The professionals who manage startup finances (bookkeepers and fractional CFOs) spend a disproportionate amount of time on revenue recognition and basis conversion. Futureproof automates the work they least want to do manually.

For Bookkeepers

Before Futureproof: Manually create deferred revenue journal entries for every annual contract. Maintain spreadsheet schedules tracking recognition timing. Reconcile Stripe payments against recognized revenue monthly. Prepare the accrual-to-cash conversion workpapers at year-end.

With Futureproof: Revenue recognition runs automatically from Stripe data. Deferred revenue balances are always current. Monthly close is reduced from days to hours. Year-end conversion starts from clean, current accrual records instead of reconstruction.

The result: bookkeepers spend time on judgment-intensive work (complex categorization, vendor negotiations, client advisory) instead of mechanical data entry. They can serve more clients at higher value.

For Fractional CFOs

Before Futureproof: Receive month-old financials from the bookkeeper. Spend the first day of every engagement reconciling numbers. Build SaaS metrics manually in spreadsheets because the accounting software doesn't calculate them. Explain to the board why last quarter's numbers were restated.

With Futureproof: Real-time accrual-basis financials are always available. SaaS metrics (MRR, NRR, burn multiple, CAC payback) are calculated automatically from the accounting data. Board decks can be assembled from live data, not month-old snapshots. The fractional CFO focuses on strategic analysis and forward-looking guidance, the work clients actually hire them for.

For CPAs at Tax Time

The annual accrual-to-cash conversion, traditionally a multi-day exercise involving spreadsheet reconciliation across deferred revenue, prepaid expenses, and accrued liabilities, starts from clean accrual books with those balances already tracked. The CPA converts and reviews rather than reconstructs, reducing tax preparation time and cost for the client.

When to Make the Switch

Start with cash basis if:

- Pre-revenue or fewer than 20 transactions per month

- No recurring subscription revenue

- Simple business model with immediate delivery and payment

Switch to accrual (or dual-basis) when:

- You have recurring revenue with annual or multi-month contracts

- You need to calculate MRR, ARR, or deferred revenue

- You are preparing for institutional fundraising

- You manage inventory with multi-period cost matching

- Investors or board members are requesting GAAP-compliant financials

Continue filing taxes on cash basis until:

- Average annual gross receipts exceed roughly $31 million (the Section 448(c) threshold, indexed annually)

- Your CPA advises otherwise based on your specific tax situation

One more caveat: switching your tax accounting method is a formal accounting-method change filed with the IRS on Form 3115, not a toggle you flip in your software.

Most SaaS and ecommerce companies between $10K and $500K MRR are in the dual-basis zone: accrual for operations, cash for taxes. Futureproof is built specifically for this stage, automating the complexity so founders and their financial partners can focus on growing the business.

See how Futureproof compares to QuickBooks for automated revenue recognition and clean accrual books.