AI in accounting is software that performs accounting work itself, rather than waiting for a person to operate it. That means categorizing transactions, reconciling accounts, preparing journal entries, chasing invoices, capturing bills, and drafting reports. In 2026, AI reliably covers most of the execution layer of startup finance, while judgment, taxes, and final accountability stay human.

That distinction, execution versus judgment, is the single most useful lens for the whole topic. Most confusion about AI in accounting comes from lumping the two together: either overselling ("fire your accountant") or dismissing ("it's just autocomplete for bookkeepers"). The truth is more specific and more useful, especially for a startup that never had an accounting department to begin with.

What is AI in accounting?

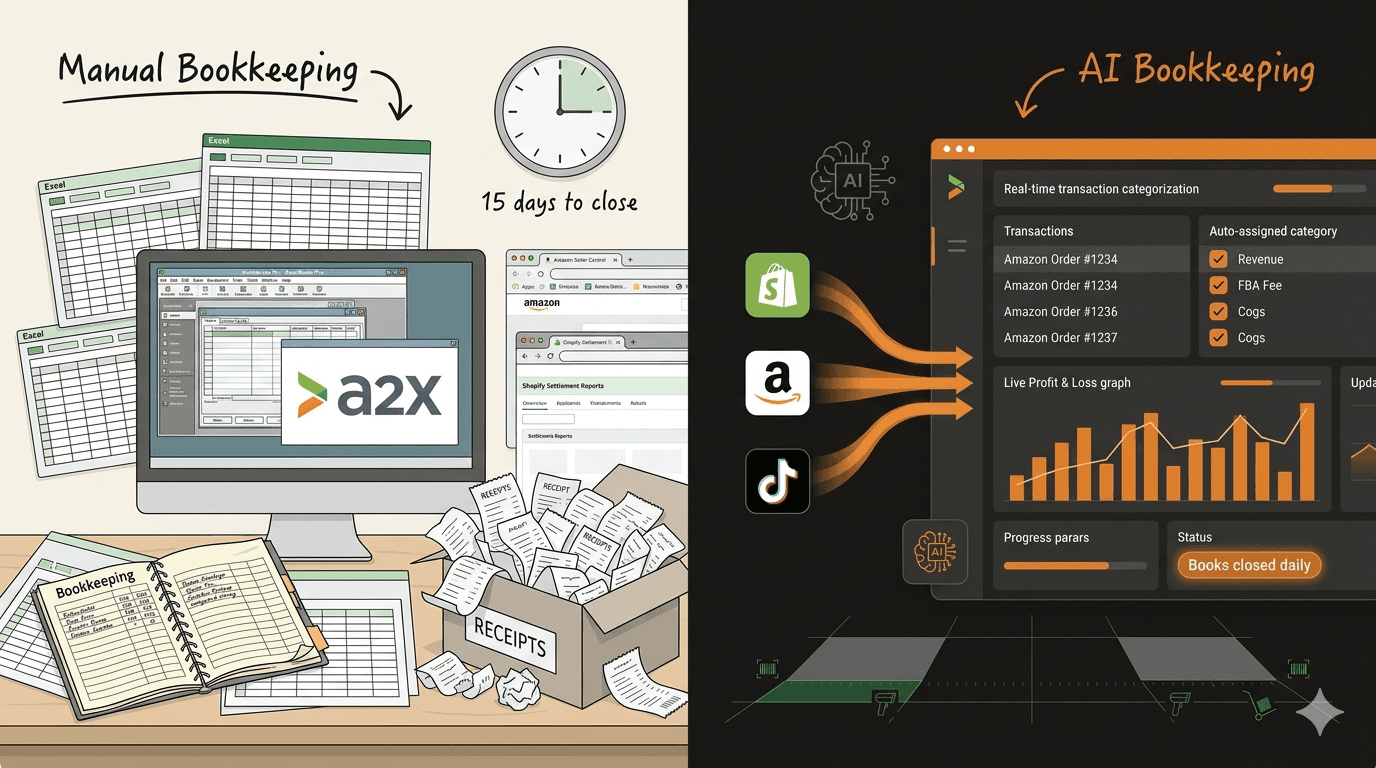

Traditional accounting software is a system of record. QuickBooks, Xero, and their peers store transactions and produce reports, but every step in between is a person's job: someone categorizes, someone reconciles, someone closes the month, someone builds the board numbers. The software is a filing cabinet with math.

AI in accounting inverts that model. The software does the categorizing, reconciling, and report-building, and the person reviews and approves. In the strongest implementations, the AI works directly on a double-entry general ledger, so every action it takes is a traceable accounting entry rather than a suggestion in a side tool. That architecture is what separates an AI finance team from a chatbot bolted onto a ledger.

What can AI do in accounting today?

The dependable use cases share two traits: high volume and clear ground truth. Where a task repeats hundreds of times a month and correctness can be checked against real data, AI performs well.

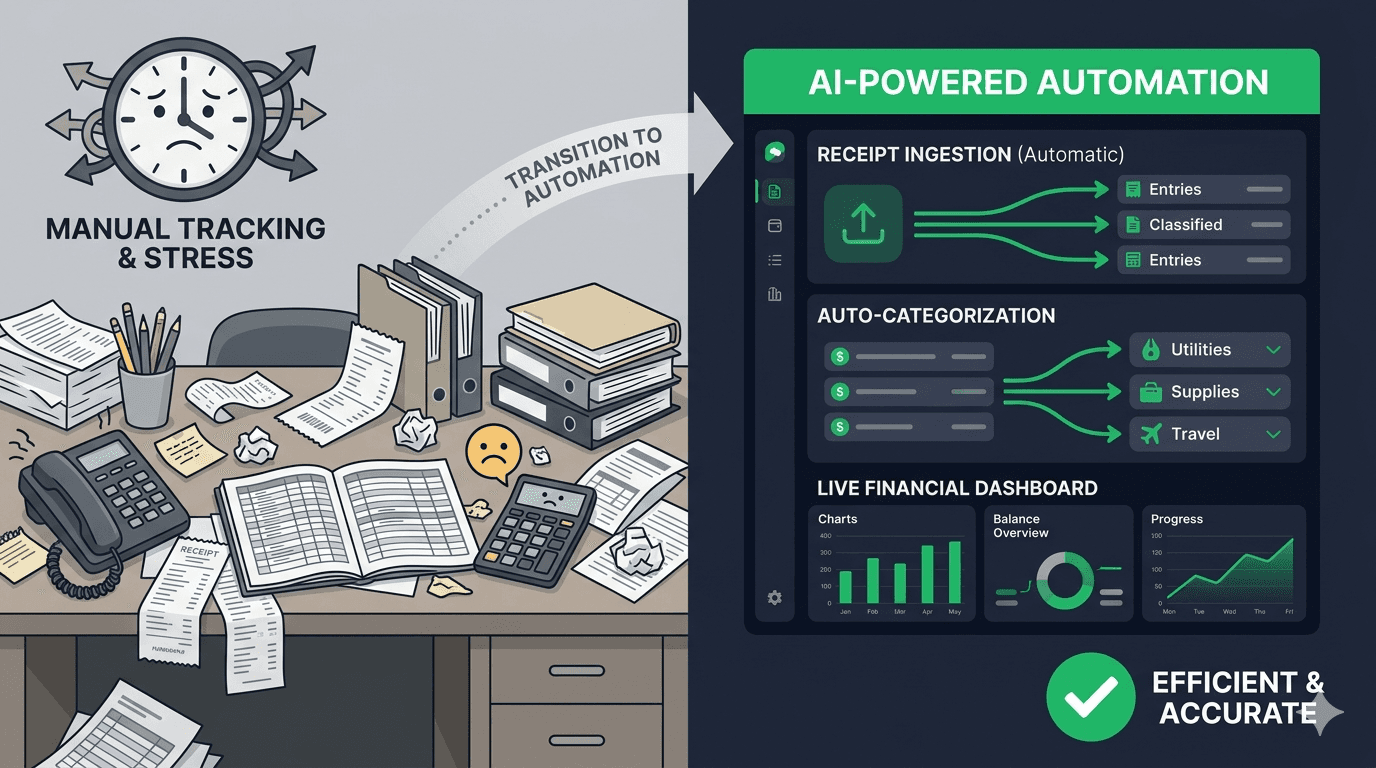

- Transaction categorization. AI reads merchant data, amounts, and history and books each transaction to the right account, learning the company's patterns. Uncertain items get flagged for a human instead of guessed. This is the core of AI bookkeeping.

- Bank reconciliation. Matching ledger entries to bank and card activity continuously, so discrepancies surface in days rather than during a month-end scramble.

- Accounts receivable. Generating invoices, matching payments, and sending collection follow-ups on a schedule a human rarely sustains.

- Accounts payable. Reading bills out of emails and PDFs, extracting terms, coding them to accounts, and preparing payment runs for approval.

- Deferred revenue schedules. Building recognition schedules from billing data and posting the monthly entries, an error-prone chore when done by hand in a spreadsheet.

- The month-end close. Running checklist items, preparing journal entries, and tying subledgers out, with a person confirming rather than compiling.

- Reporting and metrics. Computing MRR, burn, and cash runway from the live ledger and assembling investor updates from reconciled numbers instead of from exports pasted into slides.

What can't AI do in accounting?

The limits are as important as the capabilities, and they are stable enough to plan around.

Start with what happens when the AI is wrong, because it will be sometimes. A well-built system routes uncertain items to a human instead of guessing, so the ambiguous cases arrive as flags rather than errors. For the confident-but-wrong cases, continuous reconciliation is the backstop: a miscategorized transaction still has to tie out against real bank and card activity, so it surfaces as a discrepancy to fix rather than hiding in the books until year-end.

AI does not exercise judgment. It will not decide your revenue recognition policy, choose an accounting method, or tell you whether a pricing change is wise. It does not file taxes or sign audits; year-end still goes through a CPA, and anything with legal accountability keeps a human name on it. And it should never move money on its own authority. Well-designed systems use a propose-and-approve model where a person signs off on payments and unusual entries.

It is also worth saying what the labor data shows, because "AI replaces accountants" makes for better headlines than it does for forecasts. The Bureau of Labor Statistics projects employment of accountants and auditors to grow 5 percent from 2024 to 2034, faster than the average occupation, and expects automation of routine tasks to make accountants' advisory work more prominent rather than reduce demand. AI is absorbing the execution layer, not the profession.

How is AI accounting different from accounting software?

| Traditional accounting software | AI accounting | |

|---|---|---|

| What you buy | A system of record | The work plus the record |

| Who categorizes and reconciles | You, or a bookkeeper you hire | The AI, with human approval gates |

| Books are current as of | The last time someone did the books | Continuously |

| Metrics (MRR, burn, runway) | Built by hand in spreadsheets | Computed from the live ledger |

| Errors surface | At month-end, or later | When they happen, as flags |

| Cost model | Software fee plus labor | Flat fee covering the work |

The right-hand column describes what we build at Futureproof: six AI agents covering bookkeeping, receivables, payables, forecasting, revenue metrics, and investor reporting on one shared ledger, at $1,000 per month flat. The point of the table is not the product, though. It is that "AI in accounting" is an operating-model change, not a feature. Evaluating it with a software-feature checklist misses what actually changes.

How do startups adopt AI accounting?

Switching is less dramatic than it sounds: Futureproof imports your QuickBooks history from exported files, so the agents start from your real records rather than a blank ledger. The pattern that works starts with the books, because everything else depends on them. Clean, continuously reconciled books make the downstream automation trustworthy; AI forecasting or reporting layered on top of a stale ledger just produces confident nonsense faster.

From there, adoption is mostly about setting the human checkpoints deliberately. Decide what the AI may do silently (categorize a routine SaaS subscription), what it must flag (a new vendor over a threshold), and what always requires sign-off (anything that moves money). A good system makes these gates explicit. Founders who want a person reviewing the AI's work inside the product can add that too; our Human in the Loop plan pairs the agents with a dedicated finance expert at $2,000 per month, and every plan is detailed on the pricing page.

Keep the CPA. AI produces a clean, documented year-end package; the CPA turns it into filings. The two are complements, and any vendor claiming otherwise is overselling.

FAQ

What is AI in accounting? Software that performs accounting work itself, categorization, reconciliation, journal entries, AR and AP, close preparation, and reporting, with humans reviewing and approving rather than doing. It differs from traditional accounting software, which records what people do.

Is AI in accounting accurate? On high-volume execution work, yes, provided it is grounded in a double-entry ledger and flags what it is unsure about instead of guessing. Accuracy claims without an approval workflow and a traceable ledger deserve skepticism.

Will AI replace accountants? The Bureau of Labor Statistics projects accountant employment to grow 5 percent through 2034 and expects automation to shift accountants toward advisory work, not eliminate them. AI replaces execution tasks, and for startups, it covers work they were never going to hire for.

What does AI accounting cost for a startup? Point tools vary widely. Futureproof runs $1,000 per month flat for all six agents, with an optional Human in the Loop plan at $2,000 per month, versus $500 to $2,500 per month for outsourced bookkeeping alone.

The bottom line

AI in accounting is real, specific, and bounded. It does the execution layer, categorization through close through reporting, continuously and traceably. It does not do judgment, taxes, or accountability, and the vendors worth trusting say so plainly. For startups, the practical question is not whether AI will change accounting. It is whether the founder keeps doing that work at midnight, hires for it, or hands it to a system built to do it.

Start a 14-day trial of Futureproof, no credit card required, and see the execution layer running on your own books.