A founder walks into a Series A meeting with a strong deck. Revenue is up 180% year over year. The product demo lands. The lead partner nods through the growth slides, then asks one question: "What's your burn multiple?"

The founder knows their burn rate. They know their net new ARR. They've never divided one by the other. The pause lasts three seconds. It feels longer. The meeting doesn't go the way they planned.

That question wasn't a gotcha. It was the single most revealing number the investor could have asked for. And most seed-stage founders aren't ready for it.

What Burn Multiple Actually Measures

Burn multiple answers a specific question: for every dollar of new revenue you add, how many dollars are you burning to get there?

The formula is straightforward.

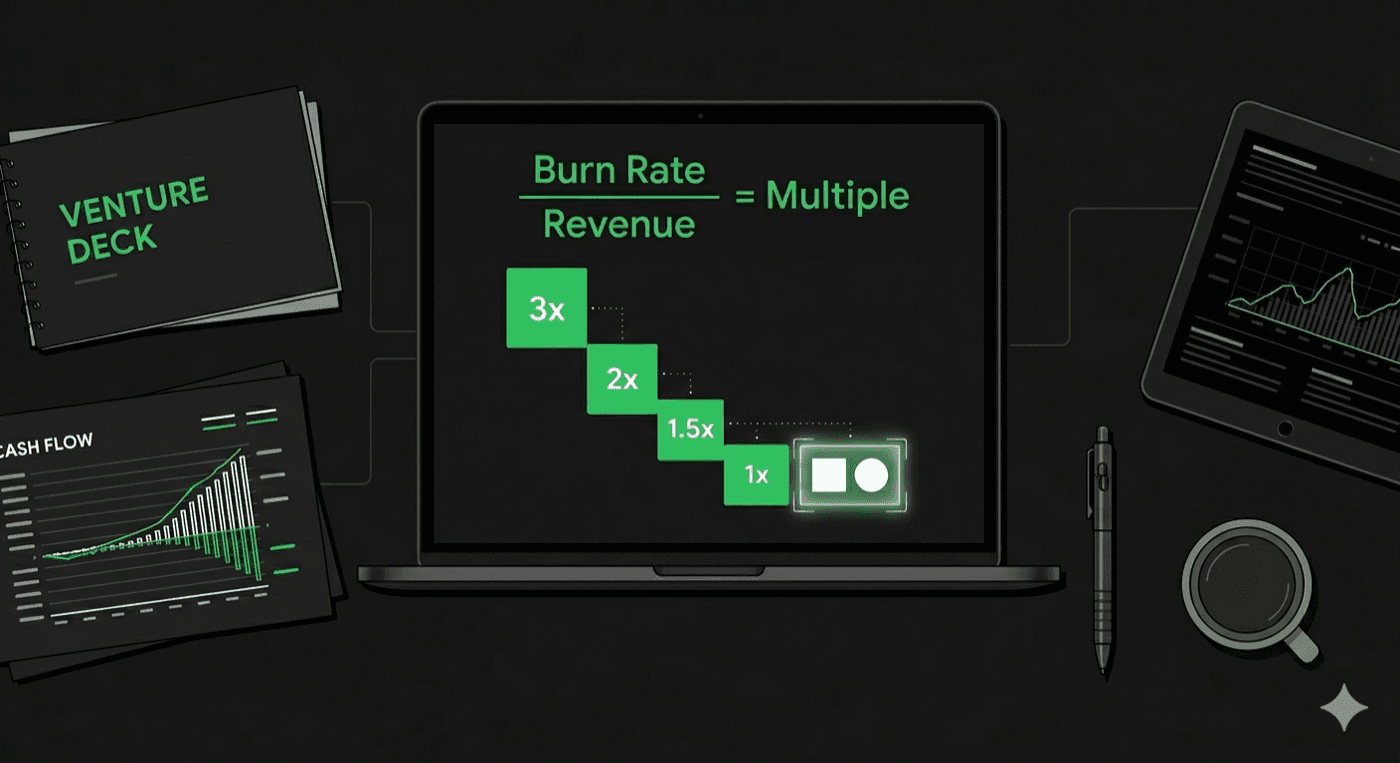

Burn multiple = Net burn / Net new ARR

Net burn is your total cash spent minus your total cash received in a given period. Net new ARR is the new annual recurring revenue you added in that same period, after accounting for churn and contraction. The distinction between gross and net matters here. If you added $150,000 in new ARR but lost $50,000 to churn, your net new ARR is $100,000. That's the number that goes in the denominator.

A realistic example. Say you're a seed-stage SaaS company. Last quarter you burned $300,000 (total spend minus total revenue collected). In that same quarter, you added $100,000 in net new ARR. Your burn multiple is 3x. For every dollar of new revenue, you spent three dollars to get it.

Put differently: at a 3x burn multiple, you'll need $3 million in capital to generate $1 million in new ARR. An investor writing a $2 million check can project exactly how far that capital goes and how soon you'll need to raise again. That projection drives their decision more than your revenue chart does.

That 3x tells an investor something your ARR growth chart doesn't. It says the growth is expensive. It means you need a lot of capital to sustain the trajectory. And it means the next round of funding will burn faster than the investor might want.

Compare that to a company growing at the same rate with a burn multiple of 1.2x. Same ARR growth, different story. The second company is building a revenue engine that almost pays for itself. The first is buying growth with cash. Investors see that distinction immediately. It shapes everything: valuation, terms, check size, and whether the conversation continues past the first meeting.

What the Benchmarks Mean

Founders who hear their burn multiple for the first time usually ask the same question: is that good? Here's the reference table investors use, whether they say it out loud or not.

Under 1x. Exceptional. You're adding more in net new ARR than you're burning. This is rare at seed stage and signals capital efficiency that investors actively seek. Companies in this range often have pricing power, strong retention, or both.

1x to 1.5x. Strong. You're burning slightly more than you're adding, but the growth engine is working. This is the range that gets Series A meetings scheduled and term sheets drafted. Investors at this level trust that the unit economics will tighten as you scale.

1.5x to 2x. Acceptable. Investors will still engage, but expect questions. They'll want to understand where the burn is going and whether you have a clear plan to bring it down. At this level, the quality of your answers matters as much as the number itself.

2x to 3x. Concerning. A burn multiple in this range tells investors that growth is expensive and potentially unsustainable. They'll discount your top-line growth rate and model out how quickly you'll need to raise again. Valuation negotiations get harder. Terms get less favorable.

Above 3x. Red flag. At this level, you're spending three or more dollars for every dollar of new revenue. Institutional investors will pass or offer terms that reflect the risk. The math is simple: if you need $3M to generate $1M in new ARR, you'll need to raise frequently, and each raise dilutes you further.

These benchmarks aren't arbitrary. They map directly to investor risk. A high burn multiple means you need more capital to hit the next milestone. More capital means more dilution. More dilution means lower returns for every dollar deployed. Investors do that math before they do anything else. That's why it's the question they ask before they dig into your ARR growth.

The Two Levers That Move It

Founders who discover their burn multiple is too high usually reach for the same lever first: cut costs. Sometimes that's the right move. But it's not the only one, and it's often not the fastest.

Go back to the formula. Burn multiple equals net burn divided by net new ARR. There are two inputs. You can change either one.

Lever 1: Reduce net burn. This means cutting expenses. Hiring slower, reducing ad spend, renegotiating vendor contracts, deferring that infrastructure project. If your burn is $300,000 and you cut it to $150,000 while holding net new ARR at $100,000, your burn multiple drops from 3x to 1.5x. That's a meaningful improvement.

But cutting burn is slow. Layoffs take time and damage morale. Vendor renegotiations take cycles. And if you cut too aggressively in areas that drive acquisition, you can hurt the denominator (net new ARR) at the same time, which means the ratio barely moves or gets worse.

Lever 2: Increase net new ARR. This means growing revenue faster without proportionally increasing spend. If your burn stays at $300,000 but you add $200,000 in net new ARR instead of $100,000, your burn multiple drops from 3x to 1.5x. Same result, different path.

How do you increase net new ARR without increasing burn? Three common approaches. First, improve net revenue retention. Expansion revenue from existing customers costs far less than acquiring new ones. If your existing base is expanding through upsells or usage growth, your net new ARR rises without a proportional increase in CAC. Second, reduce churn. Every customer you lose subtracts from net new ARR. Cutting churn by even a few percentage points can meaningfully change the denominator. Third, improve sales efficiency. Shorter sales cycles, higher close rates, and better lead qualification all increase revenue per dollar of sales spend.

The right answer depends on your business. But the strategic question is: which lever is faster? Founders who have done the math on both sides make better decisions in board meetings and investor conversations. Founders who default to "we need to cut costs" without modeling the revenue side often miss the faster path.

There's also a signaling dimension. Investors prefer the revenue lever. A founder who improved their burn multiple by growing net new ARR from $100K to $200K per quarter tells a more compelling story than a founder who improved it by cutting burn from $300K to $150K. Both result in the same 1.5x number. But the first signals a business that's figured out distribution. The second signals a business that got smaller. When you're raising, the narrative around the number matters almost as much as the number itself.

When to Calculate It and How Often

Quarterly is the minimum. Monthly is better.

Burn multiple moves faster than most founders expect. A single large deal closing can swing the number dramatically in one direction. A surprise churn event or an unplanned hire pushes it the other way. Founders who only calculate it quarterly can miss a deteriorating trend for months before it shows up in their fundraising conversations.

Monthly tracking gives you two things. First, pattern recognition. You can see whether your burn multiple is improving, stable, or getting worse over a three to six month window. That trend line matters to investors as much as the current number. A burn multiple of 2.5x that's been dropping steadily from 4x tells a different story than a 2.5x that's been climbing from 1.5x.

Second, monthly tracking gives you response time. If a bad month pushes your burn multiple above your target range, you have 30 days to course-correct before the next data point. If you're tracking quarterly, that same problem might compound for 90 days before you see it. By then, it's a fundraising liability instead of an operational adjustment.

The worst time to calculate your burn multiple is in a pitch meeting. If an investor asks and you don't know the answer, you've told them something about how you run the business. And what you've told them isn't good.

One more thing worth tracking alongside the raw number: the composition of your net new ARR. Is it coming from new logos or from expansion within existing accounts? A burn multiple of 1.5x powered by expansion revenue is structurally different from a 1.5x powered entirely by new customer acquisition. Expansion is cheaper to generate and more durable. Investors who see a strong expansion component will be more confident the number holds as you scale. If your net revenue retention is above 110%, that context makes your burn multiple story significantly stronger.

Calculate It Right Now

This isn't a post that ends with a list of things to think about. It ends with one action.

Open your financials from last quarter. Pull your total cash out and total cash in. Subtract to get net burn. Pull your ARR at the start of the quarter and your ARR at the end. Subtract to get net new ARR. Divide net burn by net new ARR.

Write the number down.

If it's under 1.5x, you're in a strong position. Keep tracking it monthly to make sure it stays there. If it's between 1.5x and 2x, you have work to do, but the path is clear. Model both levers and decide which one moves faster for your business. If it's above 2x, the next round is going to be harder than you think unless you move that number before you start the conversation.

Investors will calculate it from your financials whether you present it or not. Better to know it first, know the trend, and know your plan to improve it. That's the difference between a founder who gets the question and stumbles, and a founder who gets the question and owns the answer.

Burn multiple is one of 15 dimensions VCs evaluate before writing a check. Take our free Startup Fundraising Scorecard to see how you score across all of them (team, traction, financial clarity, and fundraising readiness) in 5 minutes.

Futureproof calculates your burn multiple automatically from your live financial data and benchmarks it against Series A expectations. No spreadsheet required.