Account reconciliation is the process of comparing balances in your general ledger against an independent record, a bank statement, a card statement, a payment processor report, and resolving every difference. It is how you prove the books reflect reality. Unreconciled books can look complete and still be wrong, which is why reconciliation is the backbone of a trustworthy close.

For founders, the word tends to arrive attached to dread, usually around month-end. It does not need to. Reconciliation is mechanically simple; what makes it painful is doing a month of it at once. This guide covers what it is, which accounts need it, the actual bank rec workflow, and how the work changes when it runs continuously instead of in a monthly binge.

Why does reconciliation matter for a startup?

Because every number you rely on inherits its credibility from it. Cash runway is only as accurate as the reconciled cash balance underneath it. Board metrics computed from unreconciled books are guesses in a nice font. And investors' diligence teams treat reconciliation quality as a proxy for whether the company's numbers can be trusted at all. They also test the control around it: the person who prepares a reconciliation should not be the only one who reviews it, and that preparer-reviewer separation is one of the first things diligence checks.

There is also a simple error-economics argument: a duplicate transaction or a missed bank fee costs seconds to fix in the week it happens, and can cost hours three months later when it has propagated into reports someone already acted on. Reconciliation is the mechanism that keeps errors young and cheap.

Which accounts need reconciling?

More than the bank account, though that is the anchor. A startup's reconciliation map usually looks like this:

| Account | Reconcile against | Typical frequency | What goes wrong here |

|---|---|---|---|

| Bank accounts | Bank statements / feeds | Continuous or monthly | Missing fees, duplicate entries, timing gaps |

| Credit cards | Card statements | Continuous or monthly | Uncategorized charges, refunds not matched |

| Payment processor (e.g., Stripe) | Processor payout reports | Monthly | Payouts booked gross vs net of fees |

| Accounts receivable | AR subledger / invoices | Monthly | Payments not applied to invoices |

| Accounts payable | AP subledger / bills | Monthly | Bills paid but still showing open |

| Payroll clearing | Payroll provider reports | Every run | Withholding and benefit splits mismatched |

| Deferred revenue | Recognition schedule | Monthly | Ledger balance drifting from the schedule |

If the last two rows look unfamiliar, that is normal at pre-seed and increasingly expensive after it. Each subledger that ties out cleanly is one less surprise during the month-end close.

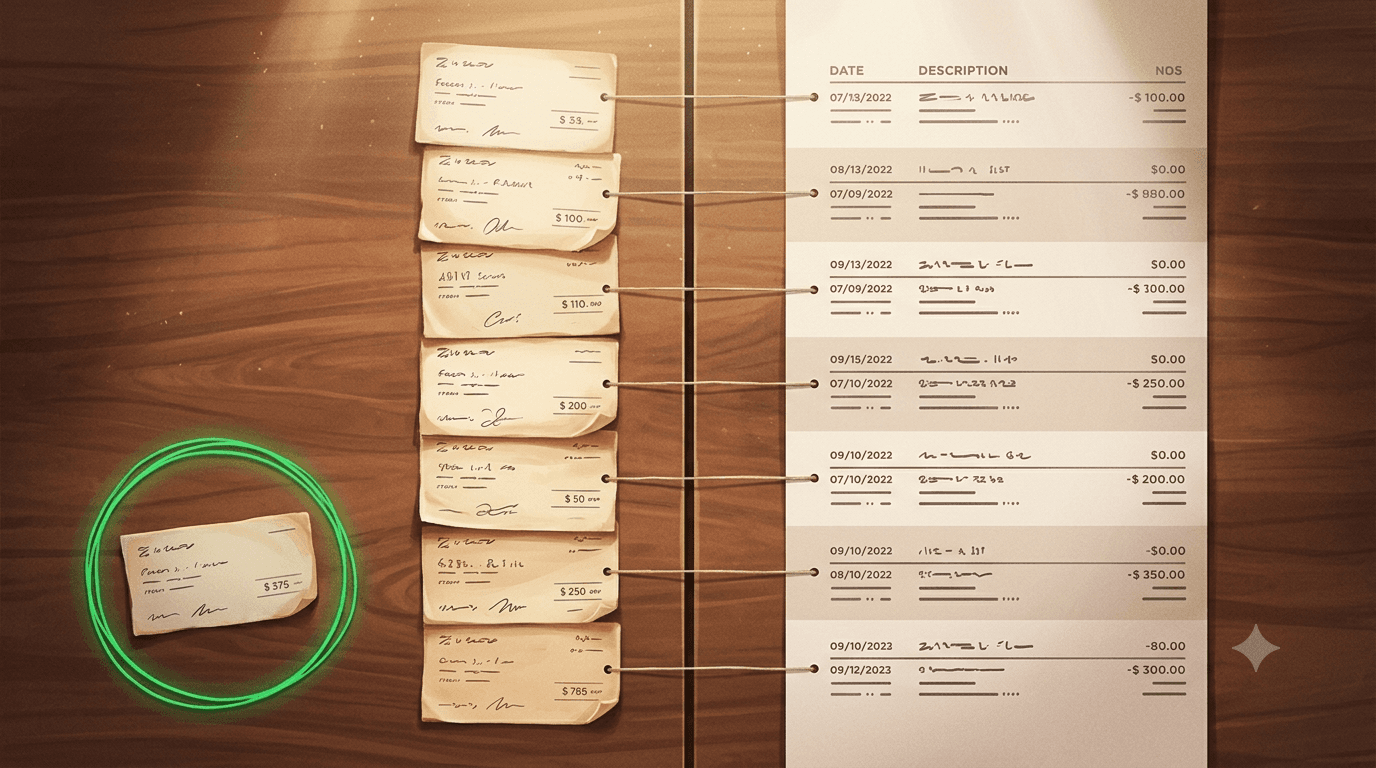

How do you do a bank reconciliation, step by step?

The classic workflow, whether done in software or on paper:

- Set the period and pull both records. The ledger's cash account activity and the bank statement for the same window.

- Match transactions one-to-one. Every ledger entry pairs with a statement line. Most modern tools auto-match the bulk on amount and date.

- List what's left on each side. Statement lines with no ledger entry (bank fees, interest, a forgotten autopay) and ledger entries with no statement line (checks not cleared, deposits in transit, duplicates).

- Resolve each difference. Record the missing items with a proper journal entry, remove duplicates, and leave true timing differences documented as reconciling items. Watch the age of those items too: an outstanding check that stays outstanding for months needs follow-up, whether that is reissuing it, voiding it, or eventually working through state escheatment rules.

- Confirm the adjusted balances agree. The adjusted book balance must equal the adjusted bank balance: the statement balance adjusted for outstanding checks, deposits in transit, and any other documented reconciling items. Save the reconciliation report; it is audit evidence, not scratch paper.

The judgment lives in step 4. Everything else is matching, which is exactly why it automates so well.

How often should you reconcile?

The traditional answer is monthly, as part of the close. The better answer is: as continuously as your tooling allows, with a formal tie-out at month-end. APQC's research on closing processes recommends reconciling complex accounts monthly precisely so issues never pile up into a year-end excavation, and the same logic applies down the calendar: weekly beats monthly, and daily beats weekly. The close stops being a discovery process when nothing is discovered there.

What changes when AI does the reconciliation?

The matching, which is most of the work, stops being anyone's job. An AI finance team matches ledger entries to bank and card feeds as transactions land, books the routine differences, and flags only the genuine exceptions, a variance it cannot explain, a duplicate it wants confirmed, for human review. At Futureproof this is Vic's work: continuous matching against live feeds, exceptions surfaced as questions rather than buried in a workbench, and a clean tie-out ready when the close starts. It is included in the $1,000 per month flat plan, and paired with close software practices, it converts reconciliation from a monthly event into a background property of the books.

What stays human is unchanged: approving unusual adjustments, deciding how to treat a genuinely ambiguous item, and owning the sign-off.

FAQ

What is account reconciliation in simple terms? Comparing your books against an independent record of the same activity, like a bank statement, finding every difference, and fixing or documenting it. It proves the books match reality.

What is the difference between bank reconciliation and account reconciliation? Bank reconciliation is one type: cash accounts against bank statements. Account reconciliation is the general practice, covering cards, payment processors, AR, AP, payroll clearing, and deferred revenue.

How often should a startup reconcile its accounts? Continuously where tooling allows, with a formal monthly tie-out at close. Monthly is the minimum; anything less lets errors compound quietly.

Can reconciliation be fully automated? The matching can be, and mostly is; well-built AI flags what it cannot confidently match instead of guessing. The review of genuine exceptions and the final sign-off stay human.

The bottom line

Reconciliation is not accounting busywork. It is the proof layer under every number a startup shows its board, and the reason a five-day close is possible at all. Do it continuously and it becomes invisible; do it monthly and it becomes the close's longest chore; skip it and every report becomes a hope.

Start a 14-day trial of Futureproof, no credit card required, and watch your accounts reconcile themselves as transactions land.