FIFO (first in, first out) assumes you sell your oldest inventory first, so your cost of goods sold reflects older purchase prices. LIFO (last in, first out) assumes you sell your newest inventory first, so COGS reflects recent prices. When costs are rising, FIFO shows higher profit and higher taxes. LIFO shows lower profit and lower taxes.

That is the difference between FIFO and LIFO in one paragraph. The harder question is which one an ecommerce brand should actually use, and in 2026, with tariff-driven cost increases moving through most import categories, the answer matters more than it has in years. This guide walks through both methods from an operator's chair, with a worked example, the US tax rules, and the third option most sellers land on.

For the full picture of how inventory valuation fits into your books, see our complete guide to ecommerce accounting.

What FIFO and LIFO actually decide

FIFO and LIFO are cost flow assumptions, not warehouse procedures. They decide which purchase costs get assigned to cost of goods sold when a unit sells, and which costs stay on your balance sheet as ending inventory. Your 3PL or Amazon FBA will rotate physical stock oldest-first regardless of what your books say, and that is fine. The accounting method and the physical flow do not have to match.

This matters because you rarely pay the same landed cost twice. Freight rates move, suppliers reprice, tariffs land, and exchange rates shift. Every purchase order creates a cost layer, and FIFO vs LIFO is the rule for which layer gets expensed first.

Under FIFO, the oldest layer is expensed first. In a rising-cost environment, that means cheaper units flow into COGS, gross margin looks stronger, and ending inventory is valued at your newest, highest costs. Under LIFO, the newest layer is expensed first, so COGS tracks what replacement inventory actually costs today, profit looks thinner, and the balance sheet carries old, low-cost layers that can sit there for years.

FIFO vs LIFO at a glance

The table below assumes rising costs, which has been the operating reality for most importing brands since the 2025 tariff rounds took effect.

| FIFO | LIFO | |

|---|---|---|

| COGS when costs rise | Lower (oldest, cheapest units expensed first) | Higher (newest, priciest units expensed first) |

| Reported gross profit | Higher | Lower |

| Ending inventory value | Higher, close to current replacement cost | Lower, built on old cost layers |

| Tax effect when costs rise | Higher taxable income | Lower taxable income |

| US GAAP / IRS status | Allowed | Allowed, with the LIFO conformity rule |

| IFRS status | Allowed | Banned under IAS 2 |

| Best fit | Most ecommerce brands, anyone seeking clean margins per SKU | Domestic businesses with large, stable inventories optimizing for tax deferral |

Two rows deserve emphasis. LIFO is legal in the United States under both GAAP and IRS rules, but the LIFO conformity rule (IRC Section 472) requires that if you use LIFO on your tax return, you must also use it in your financial statements. And IFRS prohibits LIFO entirely, so any seller with an international entity that reports under IFRS, or one planning to raise from investors who expect IFRS-comparable statements, is effectively limited to FIFO or weighted average.

A worked example with rising landed costs

Numbers make the difference concrete. The figures below are an illustration, not benchmarks, but the cost trajectory will look familiar to anyone importing in 2026.

Say a kitchenware brand buys the same SKU three times in a quarter, and tariff and freight increases push the landed cost up with each order:

| Purchase lot | Units | Landed cost per unit | Lot total |

|---|---|---|---|

| March | 500 | $8.00 | $4,000 |

| May | 500 | $9.50 | $4,750 |

| June | 500 | $11.00 | $5,500 |

| Total | 1,500 | $14,250 |

The brand sells 800 units during the quarter at $29 each, for $23,200 in revenue. Here is what each method reports:

| FIFO | LIFO | Weighted average | |

|---|---|---|---|

| COGS | $6,850 | $8,350 | $7,600 |

| Gross profit | $16,350 | $14,850 | $15,600 |

| Gross margin | 70.5% | 64.0% | 67.2% |

| Ending inventory (700 units) | $7,400 | $5,900 | $6,650 |

The math: FIFO expenses all 500 March units at $8.00 plus 300 May units at $9.50. LIFO expenses all 500 June units at $11.00 plus 300 May units at $9.50. Weighted average divides the $14,250 total spend by 1,500 units for a $9.50 unit cost.

Same units, same sales, and a $1,500 swing in reported COGS, which is 6.5 points of gross margin on one SKU in one quarter. Multiply that across a 200-SKU catalog and the method choice changes how profitable every product looks, which reorders you fund, and what you owe the IRS.

The US tax rules, stated plainly

The tax facts are frequently mangled in forum threads, so here they are as of 2026:

- LIFO is legal for US taxpayers. You elect it by filing IRS Form 970 with the tax return for the year you adopt it.

- The LIFO conformity rule applies. Use LIFO for tax and you must use it for your books and any financial statements you show lenders or investors. You cannot show investors FIFO profits and the IRS LIFO profits.

- IFRS bans LIFO. IAS 2 has prohibited it since 2005, which makes LIFO a US-only method in practice.

- Switching methods requires IRS consent. Changing your inventory method generally means filing Form 3115 for a change in accounting method. This is routine but not free, and it is not something to redo every year.

The practical read: LIFO's tax deferral is real when costs keep rising, but it comes bundled with conformity, layer tracking, and the risk of LIFO layer liquidation, where dipping into old cheap layers in a stockout year causes deferred income to come due at once. For a lean brand without a controller, that administrative weight usually outruns the benefit.

FIFO or LIFO for ecommerce sellers?

For most ecommerce brands, FIFO or weighted average is the defensible answer, and LIFO is the exception. Three reasons drive that.

First, your reporting stack assumes it. Shopify stores a single "cost per item" field per variant, not dated cost layers, and Amazon's reports give you fees and units but no cost accounting at all. Channel dashboards approximate something close to a current-cost or average-cost view. Rebuilding LIFO layers on top of that data is manual work your platform will not do for you, which is one reason ecommerce bookkeeping done properly starts from purchase records rather than channel reports.

Second, the number that runs an ecommerce business is per-SKU margin, and FIFO keeps it interpretable. When you review product profitability, FIFO ties each sale to a real purchase lot in roughly the order you bought it. LIFO can leave 2023 cost layers under your 2026 sales, which makes SKU-level decisions harder to trust.

Third, the choice only means anything if your cost inputs are right. FIFO applied to incomplete costs still overstates margin. Duties, freight, and inspection fees have to reach each unit before any method produces a true number, which is the subject of our guide to true landed cost per SKU. The same logic applies to marketplace fees eating the revenue side; our ecommerce fee calculators show what each channel actually takes.

One caveat: all of this presumes accrual books, where inventory sits as an asset until sold. If you are still cash basis, method selection is premature; see accrual vs cash basis for why inventory businesses outgrow cash accounting quickly.

Weighted average, the pragmatic third option

Weighted average cost (WAC) deserves more attention than most FIFO vs LIFO articles give it. It recalculates a blended unit cost across all layers, $9.50 in the example above, and expenses every sale at that figure. It is allowed under both US GAAP and IFRS, it smooths out lot-to-lot price noise, and it is the default in much of the inventory software market for exactly that reason.

The tradeoff is resolution. WAC blurs the lot-level detail that tells you a specific June reorder was underwater, and in a fast-rising cost environment the average lags your true replacement cost. Brands that negotiate hard on every PO tend to prefer FIFO for the visibility. Brands with high inventory turnover and stable supplier pricing often find WAC accurate enough and far simpler.

A reasonable rule of thumb: FIFO if per-lot economics drive your decisions, WAC if simplicity wins, LIFO only if your CPA models a material tax deferral and you accept the conformity and layer-tracking overhead.

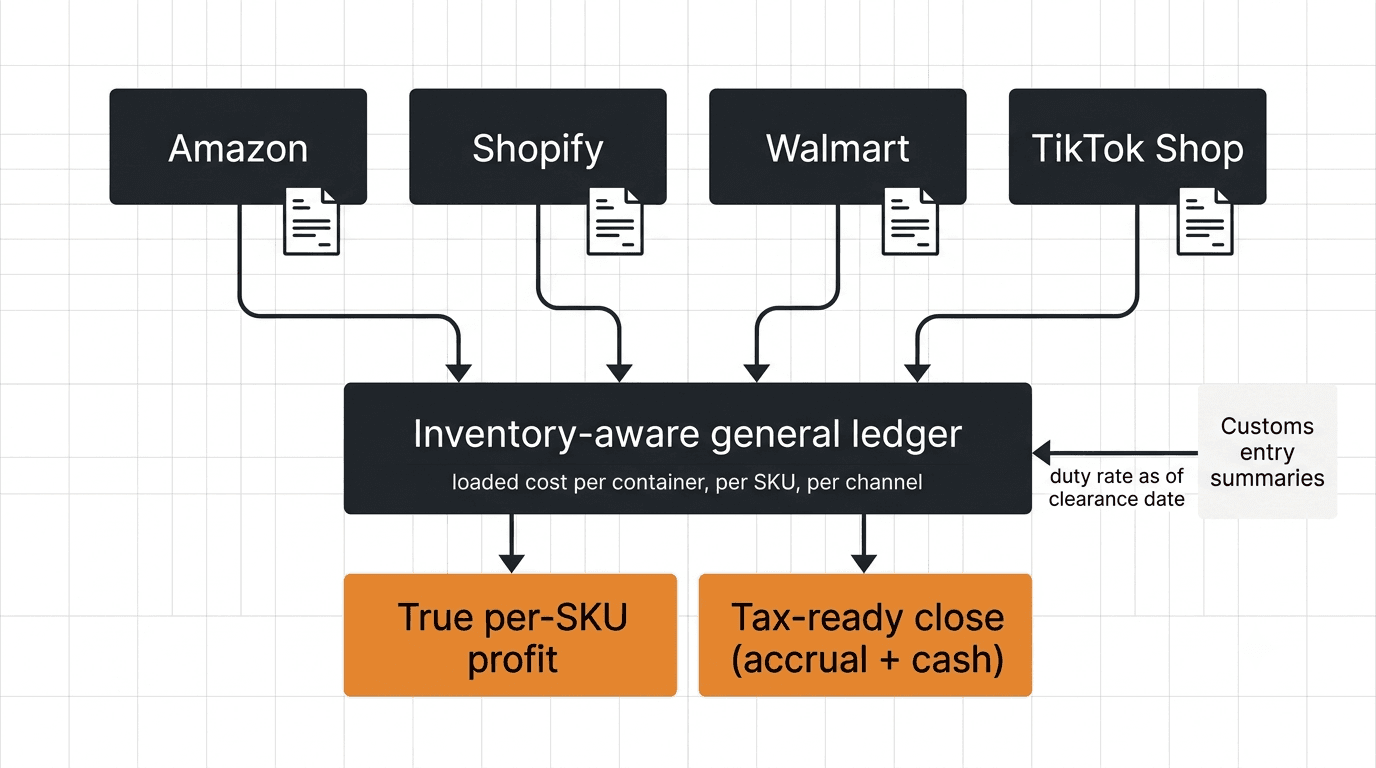

Where Futureproof fits

Whichever method you choose, it only works if every purchase cost actually lands in your books at the SKU level. That capture work is what usually breaks down, not the method itself.

Futureproof's AI finance team handles that layer. Theo captures costs from supplier and freight bills as they arrive, so each inventory lot carries its real cost, and Vic keeps inventory-aware books with per-SKU cost tracking so your COGS and margins reflect the method you picked instead of a guess. Shopify and Amazon integrations are now in beta.

If you want your inventory accounting handled by a finance team instead of a spreadsheet, join the ecommerce waitlist.

Frequently asked questions

Which is better for taxes, FIFO or LIFO?

When costs are rising, LIFO produces higher COGS and lower taxable income, so it defers tax. That advantage reverses if your costs fall, and it comes with the LIFO conformity rule, Form 970 election, and ongoing layer tracking. For most small and mid-sized sellers, the compliance overhead outweighs the deferral, which is why FIFO remains the common choice.

Can you switch between FIFO and LIFO?

Yes, but not casually. Adopting LIFO requires filing IRS Form 970, and changing an established inventory method generally requires IRS consent via Form 3115. Auditors and lenders also expect consistency between periods, so treat the method as a long-term commitment rather than an annual optimization.

What do Shopify and Amazon sellers actually use?

Most use FIFO or weighted average cost. Shopify's cost-per-item field and Amazon's reports do not track dated cost layers, so those platforms pair naturally with average-cost or FIFO bookkeeping built from purchase records. LIFO is rare in ecommerce because of the manual layer tracking and the IFRS ban for internationally reporting entities.

Is LIFO illegal?

No. LIFO is permitted for US companies under US GAAP and by the IRS, subject to the conformity rule. It is banned under IFRS (IAS 2), so companies that report internationally cannot use it, which is why it survives almost exclusively in the United States.

Does FIFO mean I have to physically sell old stock first?

No. FIFO is a cost flow assumption for your books, not a warehouse rule. Your 3PL or FBA will usually rotate old stock out first anyway for practical reasons, but your accounting method and physical picking order are independent choices.