Importing brands used to be able to set a landed cost in a spreadsheet at the start of the year and revisit it after the next shipment. Duty rates were stable enough that the input did not need a date attached. That period ended. A brand that priced a SKU last fall against a 7.5% duty line is now writing purchase orders against a duty rate that may have moved by ten points or more, on the same HTS code, between one container and the next. The selling price did not change. The marketplace fees did not change. The gross margin on every unit shipped from the new container quietly compressed, and the brand will keep selling at a margin it can no longer see until someone re-runs the math.

This is the problem the next eighteen months will keep delivering to founders and finance leads at importing private-label brands in the $5M to $50M GMV range, selling across Amazon, Shopify, and increasingly Walmart and TikTok Shop, running lean with no controller and the founder still owning the numbers. What follows covers what true landed cost has to include in a tariff environment, why timing makes the accounting harder than the math, why a single sales channel cannot answer the per-SKU profit question, and what the underlying system has to look like for the answer to stay correct between container loads.

What true landed cost actually includes

Landed cost is the all-in unit cost of a SKU at the moment it becomes sellable inventory in the channel that will ship it. For most importing brands, that means a unit ready to pick at an Amazon FBA warehouse, a 3PL serving Shopify and Walmart orders, or both. The components that compound on a per-unit basis are unit cost free on board at the supplier's port of origin, ocean or air freight allocated per unit by volumetric or cube-weight method, duties and tariffs computed on the customs value declared at entry by HTS code at the rate in effect on the date the goods arrive, customs brokerage and entry fees (including merchandise processing and harbor maintenance fees where applicable), marine cargo insurance, prep and labeling and inbound handling at a 3PL or prep center (including FNSKU labeling for Amazon), and inbound fees to the final warehouse (including FBA placement fees where the brand cannot consolidate into one destination). Most brands track unit cost and freight cleanly; the other components are where the slippage hides.

Consider a private-label kitchen accessory imported in 40-foot containers, retailing at $34.99 on Amazon. With an $8.40 unit FOB cost, $0.95 of freight per unit at a normal container fill, $0.12 of brokerage, $0.04 of insurance, $0.55 of prep at the 3PL, $0.42 of inbound to FBA, and duty at the older 7.5% rate (about $0.63 per unit), the loaded cost is $11.11. Move that duty rate to 25% on the next container, and the same SKU now lands at $12.58. The unit cost, the freight contract, and the supplier's price did not move. Duty alone moved the loaded cost by $1.47, or 13.2% of the prior landed cost.

The downstream effect lands on contribution margin in a way the dashboards do not show. At $34.99 retail with a 15% Amazon referral fee ($5.25) and a small-standard FBA fulfillment fee around $5.42, channel costs net to $10.67 per unit before any advertising. Contribution at the old landed cost is $13.21 per unit, or 37.8%. Contribution at the new landed cost is $11.74 per unit, or 33.6%. A 4.2-point compression in contribution margin, on every unit, from the date the new container clears customs. On annual sales of $500,000 for that SKU, the brand quietly gives up roughly $21,000 of gross profit it never sees leave the building, because the price tag, the Amazon report, and the bookkeeping software all still display margin as if the prior container were the source. That is the gap a moving tariff environment opens, and it opens it container by container.

Why timing is the part that breaks spreadsheets

Landed cost is not just an arithmetic problem. It is a timing problem. The money goes out long before the inventory arrives, and the costs that load onto the unit accrue in sequence over months.

A typical inbound cycle looks like this. The supplier requires a 30% deposit on order acceptance, twelve to sixteen weeks before goods ship. Production runs six to ten weeks. The supplier then ships and requests balance payment against the bill of lading, and the goods are at sea another two to six weeks depending on lane and port congestion. Customs clearance happens on arrival, with duty assessed at the rate in effect that day, against the customs value on the commercial invoice. Brokerage bills arrive a few days later. Drayage and inbound to the prep center bill on receipt. Prep and labeling bill once units are processed. Inbound to FBA or to the 3PL destination bills on the inbound shipment. Only at that point does the unit exist as saleable inventory at its final loaded cost.

Across this cycle, the brand has paid cash on multiple dates, often spanning two quarters, and accumulated cost components against units that did not yet exist as sellable inventory on any general ledger. Every one of those costs has to land on the right unit, on the right date, at the right tariff rate. A spreadsheet can keep up with one supplier and one container per quarter. A brand running two or three suppliers in rotation, importing into multiple ports, releasing units to multiple channels, will lose track of which container's costs apply to which units within two cycles. This is not a complaint about spreadsheets, it is a structural reason most importing brands cannot quote the loaded cost of a SKU on any given Tuesday without going back to source documents.

The accounting trap most brands do not see until it costs them

Inside the timing problem sits an accounting question that catches founders who built their finance setup at $1M GMV and never revisited it. When the brand pays a supplier deposit, what is that on the books?

Under accrual basis, a supplier deposit for inventory is a prepaid inventory asset on the balance sheet. It is not a prepaid operating expense, which is a separate line that covers things like rent paid in advance or annual software subscriptions. The deposit does not hit cost of goods sold. It sits in current assets until the inventory is received, at which point it converts into inventory at the full loaded cost, with the deposit applied against the supplier balance and the remaining freight, duty, brokerage, insurance, prep, and inbound fees layered on. Cost of goods sold is recognized only as those units are actually sold across channels, against the loaded cost of the container they came from.

Under cash basis, the same supplier deposit is expensed on the day it leaves the bank account. The inventory does not appear on the books as an asset, because there is no balance sheet recognition for prepaid stock in a pure cash framework. Cost of goods sold flows out when checks clear, not when units sell.

Both views are valid for their own purpose. Accrual answers decision questions: should we reorder this SKU, should we raise the price, is this category still earning its slot in the warehouse. Those questions require matching cost to revenue at the unit level, on the date the unit sold, against the loaded cost of the container it came from. Cash answers tax questions: what was actually paid and received in the period, for taxable income and quarterly estimates. Both views are legitimate, and both must run off the same underlying ledger, because the moment they drift, the brand has two truths and no way to reconcile them in front of an auditor or itself.

The difference between a healthy importing brand and a struggling one is rarely whether they keep accrual books. It is whether their cash and accrual views are computed from one inventory-aware ledger that knows which container a unit came from, what the loaded cost was on the day it cleared, and which channel sold it.

The omnichannel blind spot no single platform can fix

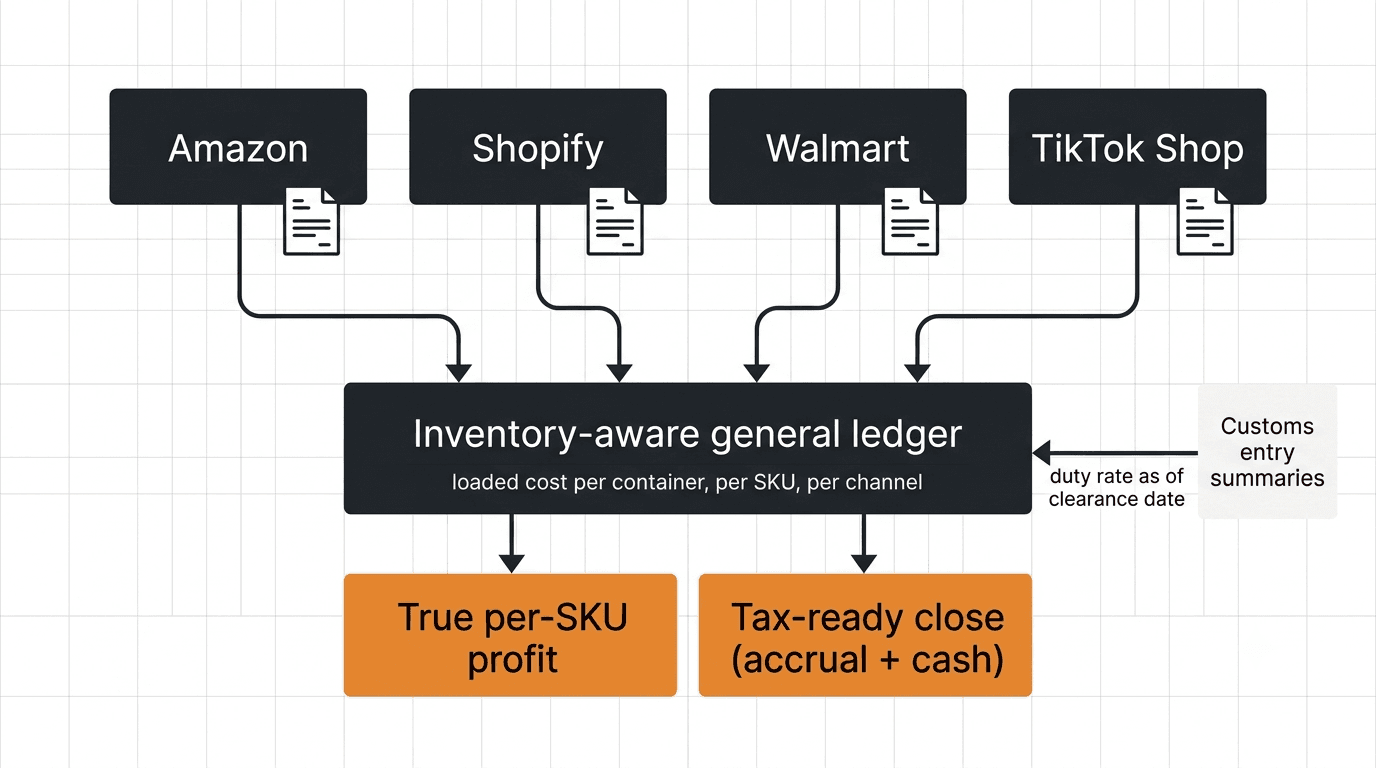

Once the loaded cost per SKU is correct, the next question is what the brand actually made on it. That question cannot be answered by any single channel.

Amazon Seller Central can produce a settlement report that shows referral fees, FBA fees, ad spend on Amazon, returns and reimbursements, and net deposit. It cannot see Shopify orders for the same SKU, ad spend on Meta or TikTok that drove Shopify checkouts, or Walmart returns coming back to the same 3PL. Shopify reports show their own orders, processing fees, and app fees, and they do not know what Amazon paid or what TikTok Shop's affiliate program ran through a different settlement window. Each platform is honest about its own slice. None of them is dishonest about the others, they simply cannot see them.

This is a structural gap, not a tooling gap. Single-channel platforms can only ever see their own data. Analytics tools that sit on top of the books inherit that same blindness, because if the underlying books do not reconcile across channels, the dashboard cannot conjure data it was never given. The only place a brand can compute true per-SKU profit is a layer that consumes settlements from every channel, allocates ad spend back to SKUs the way the channels actually attribute it, classifies returns by disposition (resellable versus not, on which channel, against which container), and matches every line against the loaded cost of the container the unit came from. Without that layer, blended COGS is an estimate, per-SKU profit is a guess, and the brand is making reorder and pricing decisions on numbers that round in different directions on different platforms.

Landed cost is a margin lever, not a hygiene task

Importing brands often treat landed cost as a finance team chore, something to clean up before tax season or before a diligence call. The leverage math says otherwise.

A dollar saved on landed cost drops, in full, to gross profit. There is no marketplace referral fee that taxes a cost reduction. There is no advertising fee that scales with the unit cost line. There is no payment processing percentage that takes a slice. Lower the duty exposure by reclassifying an HTS code defensibly, consolidate a freight lane, negotiate a deposit term that ties up less cash on prepaid inventory, swap a prep workflow that shaves 12 cents per unit, and every cent shows up in margin on the next units that hit the shelf.

A dollar added to price does not behave the same way. A $1 retail increase loses 8 to 15 cents to a marketplace referral fee depending on the channel and category. It loses additional points to higher PPC bids required to maintain the same conversion at the new price, because organic rank and click-through both shift when the price tag moves. It exposes the SKU to a measurable bump in return rate as buyer expectations shift up. The same $1 of price often nets 50 to 70 cents to gross profit, against $1 of landed cost savings that nets the full dollar.

There is a second dynamic worth noting. Margin across the consumer goods category is no longer a private number. Public filings, pitch decks, sponsored content disclosures, and ad library data make a brand's selling economics partially visible to anyone willing to read them. Visible margin signals competitive opportunity. The brand with the lowest defensible landed cost on a comparable SKU has a window: it can sell at the prevailing market price and still earn a margin that supports product development, customer acquisition, and reinvestment in the catalog. The brand whose landed cost lags has the inverse problem: every visible competitor signal narrows its options on price and on ad spend. The signal a brand projects to the rest of its category is computed off the landed cost the brand actually has, not the one it used to have.

What good looks like

The system underneath all of this has a specific shape. It is one inventory-aware general ledger that computes a loaded unit cost per SKU on the date each container clears, holds prepaid inventory deposits as assets distinct from prepaid operating expenses, recognizes cost of goods sold against the correct container at the moment of sale on each channel, reconciles settlements from Amazon, Shopify, Walmart, TikTok Shop, and any other surface the brand sells on to tax-ready accuracy, and re-computes loaded cost when a duty rate changes on the next entry. It supports accrual and cash natively, from the same underlying transaction set, so that the decision view and the tax view never drift.

Most importing brands in the $5M to $50M GMV range do not have this. They have a bookkeeping service that closes monthly on accrual, an Amazon dashboard that reports on its own data, a 3PL invoice that lands separately, a customs broker who emails entry summaries as PDFs, and a founder who reconciles the gaps in a spreadsheet the week before the board update. That setup was workable while landed cost was a static input. It is no longer workable now that tariffs have made it a moving one, across four channels that each report on their own clock.

Where did the money go

The honest version of the question every founder of an importing brand is asking is some form of "where did the money go." Revenue is up, ad spend is up, returns are within range, the books closed on time, and yet cash on hand at quarter close came in well below where the spreadsheet said it would. The answer almost always lives in the gap between what the brand thought a unit cost and what it actually cost on the container that fulfilled the orders, multiplied across channels.

Futureproof is the AI finance team that runs an inventory-aware ledger for importing multichannel brands, computing true landed cost per SKU as containers clear and reconciling true per-SKU profit across every channel the brand sells on, so the answer to "where did the money go" is on the screen before the question gets asked.