Deferred revenue journal entries follow one pattern: when a customer prepays, debit cash and credit deferred revenue (a liability); as you deliver the service each month, debit deferred revenue and credit revenue. The prepayment is not income yet, it is an obligation to deliver, and the entries move it from owed to earned as you perform.

That is the whole concept. What trips people up is the execution across twelve months, upgrades, and refunds, so this guide works the actual entries with numbers. If you want the conceptual background first, start with our deferred revenue guide; if you want the recognition framework, the ASC 606 guide covers it. This post is the debits and credits.

Why is deferred revenue a liability?

Because you owe something: twelve months of service against cash received today. Under accrual accounting, revenue is earned by delivery, not collection. Until you deliver, the customer's money is closer to a deposit than to income, and the balance sheet says so via deferred revenue. Every entry below is just that promise being kept, one month at a time.

Two presentation details a controller will expect. On multi-year prepays, split the balance into a current portion (earned within twelve months) and a long-term portion. And on the cash flow statement, the period's change in deferred revenue is an add-back within operating activities, which is how a prepay-heavy SaaS company can show operating cash flow well ahead of income.

What's the journal entry when a customer prepays?

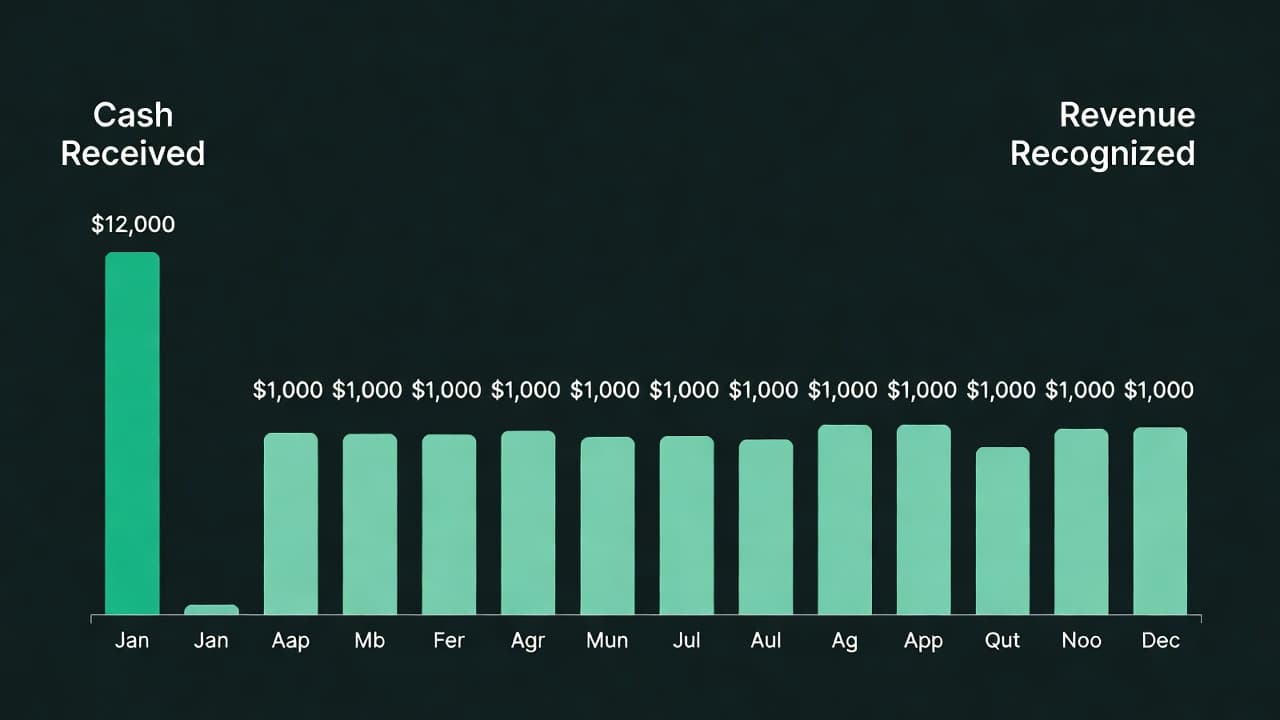

A customer signs a $12,000 annual subscription on January 1 and pays upfront:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 1 | Cash | $12,000 | |

| Jan 1 | Deferred Revenue | $12,000 |

Revenue so far: zero. If you invoice with payment terms instead of collecting immediately, the debit goes to accounts receivable first, then moves to cash when payment lands; deferred revenue is credited either way at billing. One technicality worth knowing: strictly, a receivable belongs on the books only once the right to payment is unconditional, as with a noncancellable contract, which is why practice varies on when the AR entry gets posted.

How do you recognize revenue each month?

Deliver January, earn January. At each month-end, one recognition journal entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 31 | Deferred Revenue | $1,000 | |

| Jan 31 | Subscription Revenue | $1,000 |

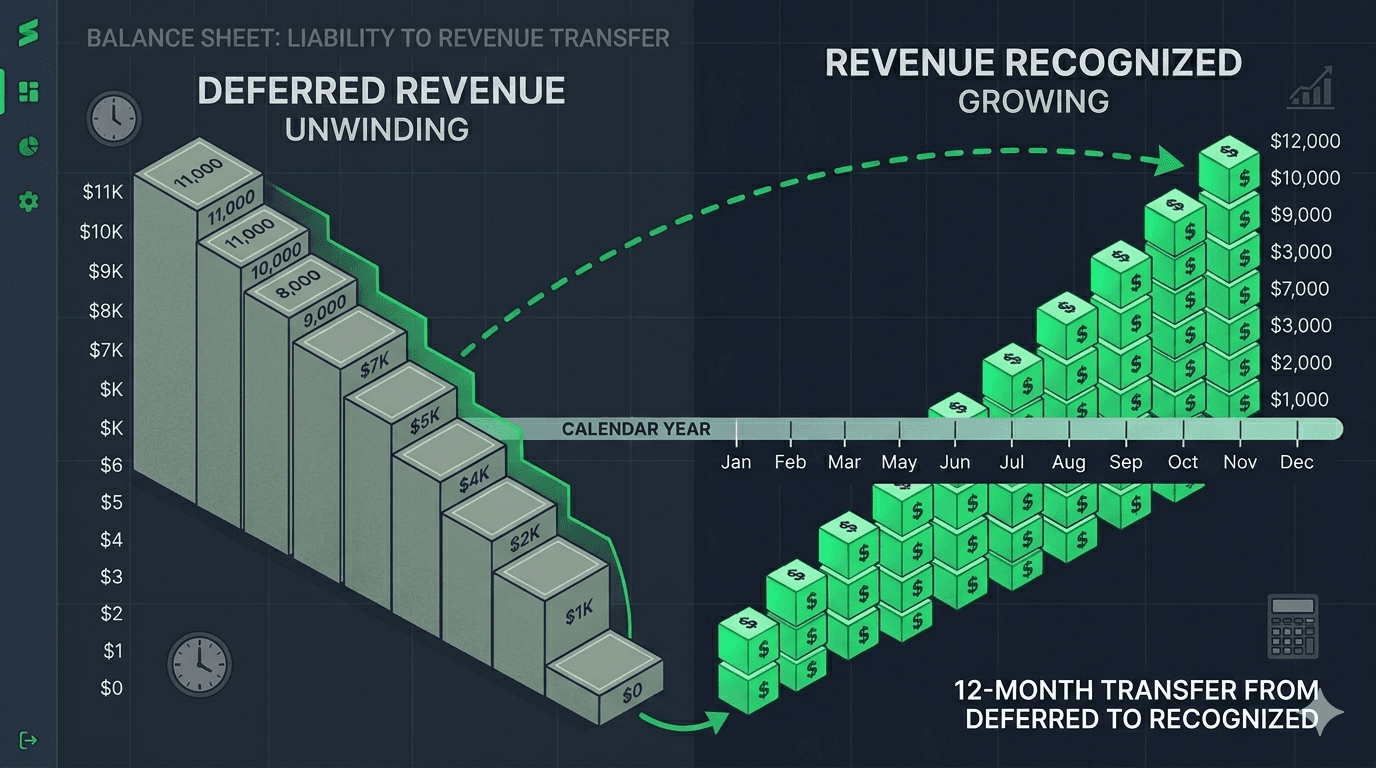

Repeat monthly. The schedule for this one contract, key months shown:

| Month | Entry | Revenue recognized (cumulative) | Deferred revenue balance |

|---|---|---|---|

| Jan | $1,000 | $1,000 | $11,000 |

| Feb | $1,000 | $2,000 | $10,000 |

| Mar | $1,000 | $3,000 | $9,000 |

| ... | $1,000/month | ... | ... |

| Jun | $1,000 | $6,000 | $6,000 |

| Sep | $1,000 | $9,000 | $3,000 |

| Dec | $1,000 | $12,000 | $0 |

By December 31 the liability is fully unwound and the full $12,000 sits in revenue, earned. Mid-month starts prorate the first entry: a January 15 start recognizes roughly $500 in January and pushes the fraction to the final period, per your proration policy, applied consistently.

What about upgrades, downgrades, and refunds?

Upgrade. On April 1 the customer upgrades, paying $6,000 more for the remaining nine months of a bigger plan. Book the new cash into deferred revenue and recognize the blended balance over the remaining term:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Apr 1 | Cash | $6,000 | |

| Apr 1 | Deferred Revenue | $6,000 |

Remaining deferred balance after March: $9,000 + $6,000 = $15,000 over nine months, so monthly recognition becomes $1,666.67 from April.

Downgrade with credit. Reduce future recognition; if you grant a credit rather than cash back, deferred revenue simply unwinds more slowly against the smaller plan, per the modified schedule.

Refund of undelivered months. Set the upgrade aside and go back to the original $12,000 contract. That customer cancels June 30 with six months undelivered and a $6,000 refund:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jun 30 | Deferred Revenue | $6,000 | |

| Jun 30 | Cash | $6,000 |

No revenue reversal is needed, because the refunded months were never recognized. That is the quiet elegance of doing this correctly: the liability always equals exactly what you still owe.

What are the most common mistakes?

- Recognizing on cash receipt. The classic error: booking the full $12,000 as January revenue. It overstates the current period, understates the next eleven, and is the first thing diligence reviewers check at a SaaS company.

- Booking the schedule but skipping the monthly entries. A spreadsheet schedule nobody posts from leaves the ledger frozen at day one.

- Letting the balance drift from the schedule. The deferred revenue account should tie to the sum of all contracts' remaining schedules every month; when it does not, reconcile before the gap compounds.

- Handling modifications by vibes. Upgrades and refunds need the remaining-term math above, not an eyeballed adjustment.

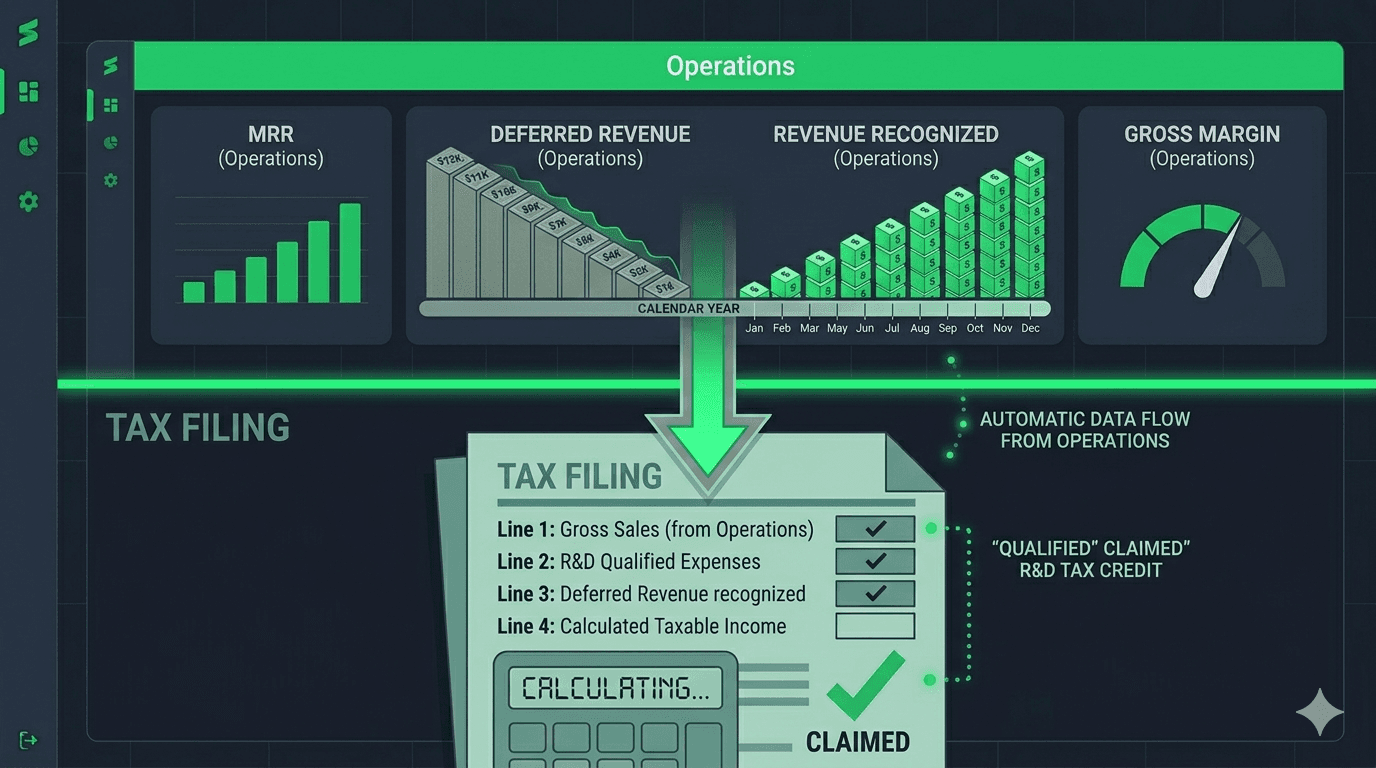

How does automation handle these entries?

Exactly as above, without the forgetting. An AI finance team builds the recognition schedule from billing data when the invoice lands, posts the monthly recognition entries automatically, adjusts schedules on upgrades and refunds, and keeps the deferred revenue account tied to the schedules so the reconciliation is continuous. At Futureproof this runs on the same ledger the rest of the bookkeeping lives on, included in the $1,000 per month flat plan, and the founder's involvement drops to reviewing anything unusual rather than remembering twelve entries per contract per year.

FAQ

What is the journal entry for deferred revenue? At prepayment: debit cash, credit deferred revenue. At each delivery period: debit deferred revenue, credit revenue for the earned portion.

Is deferred revenue a debit or credit? Deferred revenue is a liability, so it carries a credit balance. It is credited when cash is received in advance and debited as revenue is earned.

When does deferred revenue become revenue? As the service is delivered, typically ratably each month over the subscription term, regardless of when the cash arrived.

How do refunds affect deferred revenue? A refund of undelivered service debits deferred revenue and credits cash. Already-recognized months are untouched, because they were genuinely earned.

The bottom line

Deferred revenue entries are a two-step rhythm: cash in, liability up; service delivered, liability down and revenue up. Master the rhythm, keep the ledger tied to the schedules, and your revenue line stays honest through prepays, upgrades, and cancellations, which is precisely what investors are checking when they open your books.

Start a 14-day trial of Futureproof, no credit card required, and let the recognition entries post themselves on schedule.